China's April Data Collapse Accelerates Hard Landing Risks Amid Global Supply Shocks and Capital Reallocation

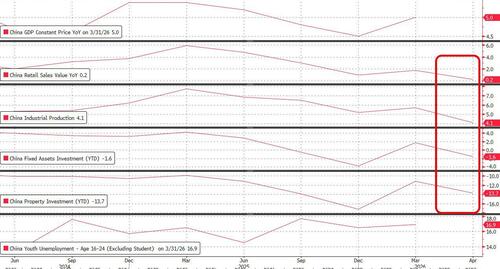

Official April 2026 data revealed industrial output at 4.1%, retail sales at 0.2%, and fixed-asset investment contracting 1.6%, confirming a severe slowdown that heightens hard-landing risks, policy dilemmas, and spillover effects on global commodities, supply chains, and capital flows.

China's official April 2026 economic readings confirmed a sharp slowdown across key metrics, with industrial production rising just 4.1% year-over-year—the weakest pace in nearly three years—retail sales growing a mere 0.2%, and fixed-asset investment contracting 1.6% in the first four months of the year. These figures, released by the National Bureau of Statistics, significantly undershot economist expectations and surprised markets already attuned to post-Covid recovery challenges and external geopolitical pressures from the Iran conflict.[1][2]

While NBS spokesman Fu Linghui described the weakness as "normal fluctuation," the breadth of the miss—retail sales at their lowest since December 2022 and investment turning negative again after a brief Q1 rebound—suggests deeper structural malaise. Property investment continued its steep decline (-13.7%), infrastructure spending slowed, and private sector confidence remains subdued despite an earlier AI-driven export surge. This aligns with a persistent imbalance between supply and demand, compounded by cautious consumers amid property sector woes and elevated inflation expectations from energy price volatility.[3][4]

Going beyond headline misses, this data collapse reinforces a hard-landing trajectory long warned about in heterodox analysis. Weak domestic demand directly feeds global supply shocks: reduced Chinese consumption of commodities helps explain softer oil balances despite supply risks, but it also signals potential downstream disruptions in manufacturing supply chains worldwide. As factories face softer orders, capital flight patterns may accelerate, with investors rotating away from China-exposed assets toward perceived safe havens or AI-themed Western equities. Legacy coverage often frames this as temporary or cyclical, yet the scale of the April deviation—even after Beijing's historical tendency to smooth data—implies the ground-level picture is worse. Economists at Nomura and others now call for stepped-up stimulus, yet the PBOC faces a policy bind: oil-driven inflation limits rate cuts, while credit demand stays weak. The July Politburo meeting will be pivotal.[5]

Connections frequently missed include the contrast with Western AI investment booms sustaining some Chinese exports while domestic demand craters, and how prolonged weakness risks exporting deflationary pressures globally. Without bolder fiscal support, this could entrench a self-reinforcing cycle of lower investment, eroded confidence, and capital outflows—far from the "resilient" narrative that persisted earlier in 2026.

LIMINAL: China's verified data collapse accelerates the hard landing scenario, driving global supply chain rebalancing, commodity demand destruction, and sustained capital flight that mainstream outlets still treat as fleeting monthly noise.

Sources (5)

- [1]China's economy loses steam in April as retail sales hit 40-year low(https://www.cnbc.com/2026/05/18/china-april-retail-sales-industrial-output-investment-unemployment-iran-war.html)

- [2]China's fixed-asset investment down 1.6 pct in first 4 months(https://english.news.cn/20260518/d6c6063bbd14460980c3918cef5691de/c.html)

- [3]China's industrial production growth slows(https://www.ft.com/content/5b1dcd37-7567-4302-9f7a-424ec7e43ee0)

- [4]China's April industrial output, retail sales growth miss expectations(https://m.economictimes.com/news/international/world-news/chinas-april-industrial-output-retail-sales-growth-miss-expectations/amp_articleshow/131165413.cms)

- [5]China Industrial Production(https://tradingeconomics.com/china/industrial-production)