Housing's False Choice: Shelter for All or Speculative Asset for the Few

Heterodox analysis reveals housing's incompatibility as both universal shelter and speculative financial asset. Corroborated by Fed research on widespread occupancy fraud, studies on STVR-driven rent/price inflation, and investigations into financialization, low rates and credit expansion enable wealthy hoarding while pricing out residents. Mainstream coverage under-interrogates this core incentive structure and its inequality-amplifying effects.

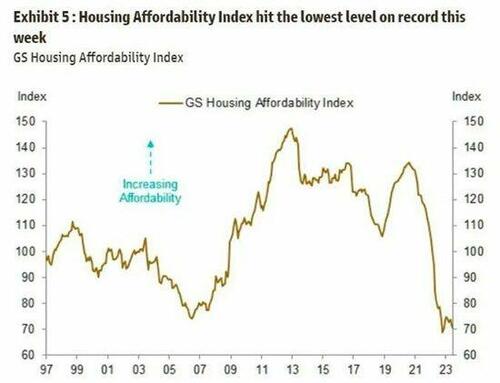

The core tension in America's housing market is rarely stated so bluntly in mainstream coverage: housing cannot simultaneously function as reliable shelter for ordinary people and as a low-risk, high-appreciation asset class in a credit-fueled bubble economy. This framing, drawn from heterodox economic analysis, reveals a financialization process that mainstream discourse often treats as neutral market evolution rather than a policy-driven choice with profound social costs.

Real-world data supports key elements of this critique. A Philadelphia Federal Reserve working paper documents pervasive owner-occupancy fraud, in which borrowers misrepresent investor or second-home purchases as primary residences to secure lower rates and better terms. Such fraud was broad-based across GSE, bank, and private loans—accounting for roughly one-third of the investor loan population—and persists beyond the 2000s housing bubble. Fraudulent 'owner-occupants' default at 75% higher rates than honest borrowers and show higher propensity for strategic default when prices stall, underscoring systemic misreporting that inflates demand statistics and masks vacancy.[1][1]

Short-term vacation rentals (STVRs) and absentee ownership amplify the shelter-asset conflict, especially in high-demand areas. Academic studies cited in housing analyses show Airbnb-style listings have raised annual rents by 1.3-2.7% in Berlin and pushed house prices up 3.7% on average in Portuguese cities—with increases exceeding 30% in the historic centers of Lisbon and Porto where conversions are concentrated. In U.S. resort towns, STVRs have converted significant shares of housing stock (sometimes 15% or more) from long-term rentals into tourist lodging, pricing out local workers and hollowing out year-round communities. What began as 'monetize your spare room' has scaled into institutional-grade capital allocation.[2]

Institutional corporate ownership of single-family homes remains relatively modest nationally (large investors hold roughly 1-3% of the stock per Urban Institute and other analyses), yet the broader pattern of wealthy individuals, LLCs, and second-home hoarding—enabled by suppressed interest rates and abundant credit—drives much of the pressure. Post-2008 and pandemic-era monetary policy channeled liquidity into real estate as a perceived safe store of value less volatile than equities. Shelterforce's 'Homes or Cash Cows?' series meticulously traces this financialization: homes increasingly serve as vehicles for speculation, wealth extraction, and portfolio diversification rather than stable shelter, exacerbating inequality, displacing residents, and linking Fed policy directly to rising prices and rents that favor existing asset holders.[3]

The deeper connection mainstream coverage misses is the feedback loop between monetary expansion, asset appreciation expectations, and restricted supply. When housing's primary purpose becomes capital preservation and leveraged gains, those needing it for shelter are structurally outbid. Brookings Institution research on housing bubbles long ago noted that viewing homes primarily as investments—expecting perpetual appreciation—detaches prices from fundamentals of shelter utility. Japan’s rigorous occupancy auditing stands in contrast to U.S. privacy norms that enable hidden vacancies and rent-controlled hoarding in cities like New York and San Francisco.

Without deliberate policy reorientation—higher carrying costs on vacant or STVR properties, tighter occupancy verification, or shifts in credit allocation—housing will remain an elite asset first and shelter second. The data show this is not inevitable market outcome but the predictable result of incentives that reward bubble participation over human need. The choice is binary, and current trajectory favors the latter.

LIMINAL: Treating housing as a primary asset class for capital parking will widen generational wealth divides, intensify social friction in unaffordable regions, and increase systemic risk from any future price correction unless incentives are deliberately realigned toward shelter utility.

Sources (5)

- [1]Owner-Occupancy Fraud and Mortgage Performance(https://www.philadelphiafed.org/consumer-finance/mortgage-markets/owner-occupancy-fraud-mortgage-performance)

- [2]Homes or Cash Cows? Series(https://shelterforce.org/series/homes-or-cash-cows/)

- [3]The Airbnb Effect: short-term rentals with long-term impacts(https://world-habitat.org/blog/airbnb-and-the-housing-crisis/)

- [4]Role of Single-Family Rentals in the U.S. Housing Market(https://www.stlouisfed.org/on-the-economy/2025/oct/role-single-family-rentals-us-housing-market)

- [5]Is There a Bubble in the Housing Market? (Brookings Papers)(https://www.brookings.edu/wp-content/uploads/2003/06/2003b_bpea_caseshiller.pdf)