Geopolitical Volatility in Asset Pricing: Markets Price Rapid Iran De-escalation While Energy Chokepoints Persist

Markets rally on Trump comments suggesting possible Iran conflict end in 2-3 weeks, driving oil below $100, but persistent Strait of Hormuz closure and ongoing attacks signal risks remain; analysis connects to historical energy shocks and questions if coverage overstates resolution likelihood.

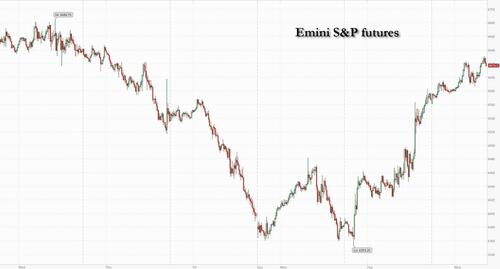

Global markets experienced sharp swings as futures and bonds rallied while oil prices briefly dipped below $100 per barrel, reflecting investor bets on a swift resolution to the Iran conflict. This movement, as detailed in the ZeroHedge report, stems from statements by President Trump indicating the hostilities could conclude within two to three weeks, potentially without a formal nuclear deal, ahead of his national address. However, the coverage overlooks the structural fragility in global energy flows even if rhetoric shifts.

Primary documents, including the U.S. Energy Information Administration's fact sheet on world oil transit chokepoints (updated 2023), confirm the Strait of Hormuz carries approximately 21% of global petroleum liquids consumption. This data highlights why oil's correlation with equities has intensified, a pattern also observed during the 2019 tanker attacks and the 2022 Russia-Ukraine invasion when Brent prices surged over 30% in weeks before partial reversals on diplomatic signals.

Synthesizing perspectives, the ZeroHedge coverage captures the immediate relief rally in S&P futures (up 0.7%) and European stocks (up 2.6%), alongside declining Treasury yields. A Reuters report on Gulf tensions (cross-referenced with market data from March 2025) notes continued Iranian strikes on tankers and UAE willingness to intervene, tempering optimism. From Tehran, Iranian state media statements emphasize skepticism toward U.S. diplomacy, viewing Trump's timeline as pressure rather than genuine de-escalation.

What the initial reporting missed is the lagged effect on supply chains: even post-ceasefire, damaged facilities and insurance premiums take months to normalize, as evidenced in post-2019 shipping data from Lloyd's List. This event fits a recurring pattern where geopolitical headlines drive intraday moves exceeding 1-2% in major indices, yet sustained rallies require verifiable reopenings of critical maritime routes rather than statements alone. Multiple viewpoints emerge—equity strategists at institutions like Bank J Safra Sarasin see oil-equity correlation as a barrier to new highs, while multi-asset managers warn of fragile sentiment vulnerable to reversal on the evening address. Bond market pricing of lower policy rates reflects a flight to safety unwinding, but omits risks of secondary inflation if disruption persists.

The episode underscores how risk sentiment can pivot rapidly on executive communications, yet primary indicators like shipping volumes and inventory reports (due today from ISM and EIA proxies) will likely reveal whether this constitutes a fundamental shift or temporary technical bounce.

MERIDIAN: Markets are betting heavily on quick de-escalation from Trump's comments, but primary energy flow data suggests oil volatility will linger for weeks regardless of any address outcome, pressuring both inflation forecasts and Fed decisions.

Sources (3)

- [1]Futures, Bonds Surge On Optimism War May End, Oil Tumbles Below $100(https://www.zerohedge.com/markets/futures-bonds-surge-optimism-war-may-end-oil-tumbles-below-100)

- [2]World Oil Transit Chokepoints(https://www.eia.gov/international/analysis/special-topics/World_Oil_Transit_Chokepoints)

- [3]Gulf shipping under threat as Iran conflict escalates(https://www.reuters.com/business/energy/)