Chevron and ConocoPhillips Sound Alarm on Oil Shortages: Geopolitical Tensions and Energy Transition Collide

Chevron and ConocoPhillips warn of 'critical' oil shortages due to the Hormuz blockade amid US-Israel-Iran conflict, predicting severe supply disruptions and demand destruction by mid-2023. Beyond corporate alerts, this crisis exposes systemic energy vulnerabilities, geopolitical risks, and energy transition gaps, with overlooked impacts on inflation, social stability, and climate goals.

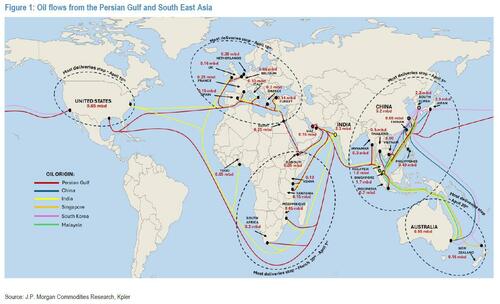

Recent warnings from Chevron and ConocoPhillips about 'critical shortages' of oil, driven by the ongoing blockade of the Strait of Hormuz amid the US-Israel-Iran conflict, underscore a deepening crisis in global energy markets. Both companies, reporting robust earnings on April 28, 2023, highlighted a supply crunch that has already pushed Brent crude prices up by over 50% in just nine weeks, with ConocoPhillips CFO Andy O’Brien predicting severe shortages for import-dependent nations by June-July. Chevron CEO Mike Wirth echoed this concern, noting on CNBC that without reestablished supply through Hormuz—through which 20% of global oil and LNG typically flows—'demand destruction' through soaring prices is inevitable. This crisis, now in its third month since hostilities escalated in late February, is compounded by an 8 million barrel per day cut in global refining capacity, impacting everything from jet fuel to fertilizers.

What mainstream coverage often misses is the broader context of systemic vulnerabilities in the global energy system. The Hormuz blockade is not an isolated event but a flashpoint in a web of geopolitical tensions, including US-Iran sanctions since 2018 and regional proxy conflicts in Yemen and Syria, which have long threatened energy corridors. The International Energy Agency (IEA) warned in its 2022 World Energy Outlook that global spare oil capacity was already at historic lows before this conflict, with OPEC+ struggling to meet demand growth. This crisis also intersects with the faltering energy transition: while renewable energy capacity grows, it cannot yet offset fossil fuel dependency in critical sectors like shipping and heavy industry, leaving economies exposed to such disruptions.

Original reporting, such as ZeroHedge’s focus on corporate earnings calls, overlooks the structural fragility of oil inventories. Chevron’s mention of inventories nearing 'operational stress levels' aligns with data from the US Energy Information Administration (EIA), which noted in March 2023 that global crude stockpiles were already 5% below their five-year average before the Hormuz closure. This suggests a miscalculation in market resilience; the 'grace period' of pre-blockade tankers cited by O’Brien has masked the true scale of impending shortages. Moreover, the narrative of 'demand destruction' as an abstract economic adjustment ignores its human cost—skyrocketing fuel prices could exacerbate inflation, already at multi-decade highs in the EU and US, disproportionately harming low-income households and potentially triggering social unrest, as seen during the 2008 oil price spike.

A critical oversight in coverage is the lack of focus on diplomatic or strategic responses. While Chevron’s Wirth mentioned ongoing talks with the Trump administration, there’s little discussion of contingency plans like tapping the US Strategic Petroleum Reserve (SPR)—already at its lowest level since 1983, per EIA data—or accelerating alternative supply routes via Saudi Arabia’s East-West Pipeline, which has limited capacity. Nor is there sufficient attention to how this crisis might reshape energy policy, potentially delaying decarbonization goals as nations prioritize short-term energy security over climate commitments, a pattern observed post-2022 Ukraine crisis when European coal use surged.

Synthesizing insights from primary sources, the IEA’s monthly oil market report (April 2023) projects a tighter supply-demand balance than previously anticipated, estimating a 2 million barrel per day deficit by Q3 if Hormuz remains closed. Meanwhile, the EIA’s Short-Term Energy Outlook (April 2023) flags that non-OPEC production, particularly in the US Permian Basin where ConocoPhillips is ramping up spending, cannot fully offset Persian Gulf losses due to logistical and investment lags. These reports, paired with corporate warnings, suggest a perfect storm of geopolitical risk and market rigidity, where even a partial resolution to the conflict may not avert price shocks or economic ripple effects.

Ultimately, this crisis reveals a deeper truth: the global energy system remains perilously tethered to volatile regions, and the transition to renewables, while accelerating, is not yet a buffer against such shocks. The intersection of geopolitics, market dynamics, and policy inertia could redefine energy security for years to come, with implications far beyond oil prices—potentially reshaping inflation trajectories, international alliances, and climate strategies.

MERIDIAN: I anticipate that if the Hormuz blockade persists beyond Q2 2023, oil prices could breach $150 per barrel, forcing significant policy shifts like emergency SPR releases or renewed coal reliance, undermining short-term climate goals.

Sources (3)

- [1]ConocoPhillips, Chevron Warn About 'Critical Shortages' Of Oil(https://www.zerohedge.com/markets/conocophillips-chevron-warn-about-critical-shortages-oil-soaring-prices-demand-destruction)

- [2]IEA Oil Market Report - April 2023(https://www.iea.org/reports/oil-market-report-april-2023)

- [3]EIA Short-Term Energy Outlook - April 2023(https://www.eia.gov/outlooks/steo/)