US Rare Earth Supply Chain Risks Extend to 2035 as Processing Dominance and Policy Divergences Shape Long-Term Market Dynamics

Analysis of US-China rare earth dependencies reveals enduring processing bottlenecks with pricing and security ramifications through 2035, drawing on official US and allied assessments.

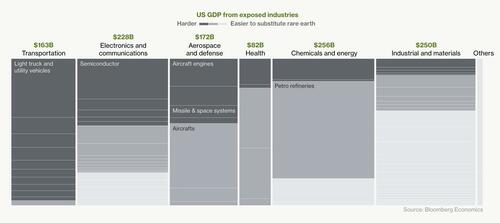

US government assessments, including the Department of Defense's 2022 supply chain review and USGS Mineral Commodity Summaries, underscore that heavy rare earth elements like dysprosium remain constrained by China's control over separation and magnet production stages, even as light rare earth projects advance in Australia and the US. Chinese state planning documents emphasize integrated industrial policy that has scaled refining capacity over decades, creating cost barriers that have historically idled non-Chinese ventures during price volatility. From a US policy lens, initiatives under the Defense Production Act and allied partnerships aim to address defense applications in magnets for F-35s and submarines, yet primary records reveal persistent gaps in domestic expertise for multi-stage chemical processing. Industry analyses contrast this with market-driven views that favor diversified sourcing to mitigate pricing spikes affecting EV motors and wind turbines. Connections to broader critical minerals strategies, such as those outlined in executive orders on supply resilience, suggest that without accelerated technology transfer restrictions or joint ventures, shortages could influence global contract pricing into the mid-2030s. The original coverage understates how export controls on processing know-how, referenced in Chinese regulatory filings, compound delays beyond simple mining output forecasts.

MERIDIAN: Structural concentration in heavy rare earth refining will sustain elevated price volatility, prompting sustained allied investment in alternative capacity through the 2030s.

Sources (3)

- [1]US Department of Defense Supply Chain Review(https://www.defense.gov/News/News-Stories/Article/Article/3110934/)

- [2]USGS Mineral Commodity Summaries 2024(https://pubs.usgs.gov/periodicals/mcs2024/mcs2024.pdf)

- [3]Executive Order on America's Supply Chains(https://www.whitehouse.gov/briefing-room/presidential-actions/2021/02/24/executive-order-on-americas-supply-chains/)