Record Sovereign Debt Flood: Structural Fiscal Explosion Ignored Amid Market Noise

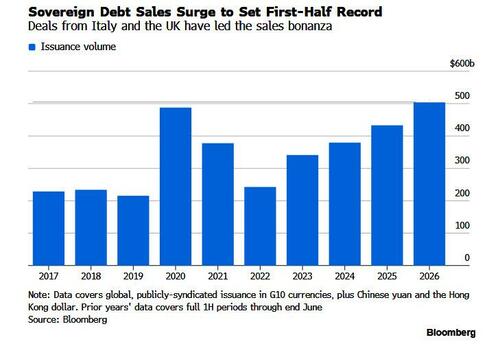

Bloomberg data reveals record $504B in syndicated sovereign bond sales in H1 2026 amid surging deficits from defense, energy transition, and demographics. OECD projections show $29T total bond issuance expected this year with heavy refinancing needs, signaling a structural shift to higher permanent debt levels that mainstream narratives minimize.

While financial media obsesses over daily yield fluctuations and central bank whispers, a deeper transformation is underway in global public finances. According to Bloomberg, governments have sold a record $504 billion in syndicated bonds so far in 2026 — surpassing even the emergency borrowing seen in the first half of 2020 during COVID lockdowns. This figure represents only the portion arranged through banks; the total sovereign borrowing picture is far larger. Italy has led the charge with nearly €70 billion ($81 billion) in the first six months, while Germany — having dismantled its longstanding 'debt brake' — raised €14 billion through syndications to fund defense and infrastructure. The UK, Belgium, Serbia, Australia, and Mexico have also executed oversized deals.[1]

The OECD's Global Debt Report 2026 projects that governments and companies will raise a combined $29 trillion from bond markets this year, with OECD sovereign borrowing alone approaching $18 trillion — much of it (around 78%) dedicated purely to refinancing existing obligations rather than new spending. This comes as global debt has climbed toward $353 trillion, driven by persistent budget deficits that have widened since the global financial crisis, exploded during the pandemic, and are now re-accelerating due to military outlays, energy transition costs, support for households amid price shocks from the Iran conflict, and demographic pressures from aging populations.[2][3]

Analysts like Jens Peter Sorensen at Danske Bank point to increased public spending on military, infrastructure, and green initiatives as the primary driver. The EU has relaxed fiscal rules to accommodate this. Demand for shorter-maturity government debt has remained resilient, allowing issuers to push forward with heavy refinancing calendars even as rates rise. Yet this 'healthy' market window masks growing vulnerabilities: a 30-year US Treasury auction in May saw yields above 5% for the first time since 2007, and UK gilts have seen elevated yields not witnessed since 2008. With central banks like the ECB preparing hikes and the Fed expected to tighten further, the stage is set for heightened sensitivity to rate spikes.

Mainstream coverage typically frames these auctions in isolation — success of one sale or another — while downplaying the structural shift toward permanently elevated debt-to-GDP ratios and the political impossibility of reversing spending commitments on defense, climate, and entitlements. This is not a temporary surge but a new baseline where refinancing risk compounds, investor bases evolve, and term premia remain elevated. Heterodox observers have long warned that such dynamics lead toward financial repression, implicit monetization, or outright revulsion when markets finally balk at absorbing 'debt that will never be repaid.' The current record pace, coinciding with geopolitical tensions in the Persian Gulf and deteriorating economic outlooks, suggests we are witnessing the early phase of a sovereign debt trap that daily market noise is designed to obscure.

LIMINAL: This record debt issuance amid rising rates and irreversible spending commitments marks a point of no return, where governments' growing reliance on rolling over ever-larger obligations will likely force central banks into sustained monetary accommodation or trigger a wave of fiscal dominance and market stress by the early 2030s.

Sources (3)

- [1]Governments Sell Bonds at Record Pace as Spending Soars(https://www.bloomberg.com/news/articles/2026-06-10/governments-are-selling-bonds-at-record-pace-as-spending-soars)

- [2]Global Debt Report 2026(https://www.oecd.org/en/publications/2026/03/global-debt-report-2026_59d2d627.html)

- [3]Sovereign Borrowing Outlook: Global Debt Report 2026(https://www.oecd.org/en/publications/global-debt-report-2026_e9d80efd-en/full-report/sovereign-borrowing-outlook_4470147b.html)