PIMCO's $10B Private Lifeline to Gulf States Exposes Liquidity Fragility Beneath Oil Wealth and Non-Bank Credit's Geopolitical Rise

PIMCO's rapid $10B+ private lending to UAE, Qatar and Kuwait amid Iran conflict highlights dollar liquidity strains in oil economies despite sovereign wealth funds. Analysis reveals faster private credit channels substituting for closed public markets, with implications for transparency, costs, and non-bank actors' rising influence in geopolitical stability.

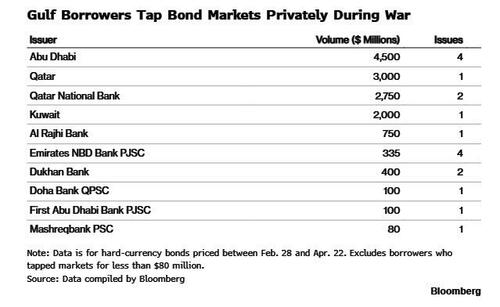

While the ZeroHedge/Bloomberg reporting accurately captures PIMCO's deployment of over $10 billion in private placements to Abu Dhabi, Qatar, Kuwait, and Qatar National Bank between late February and mid-April, it stops short of connecting this transaction flow to longer-term structural weaknesses in hydrocarbon-dependent fiscal models. Primary data from the IMF's April 2025 Middle East and Central Asia Regional Economic Outlook documents a sharper-than-expected contraction in oil revenues following Strait of Hormuz disruptions, with growth forecasts for GCC economies revised downward by an average of 1.8 percentage points. The private placements, carrying coupons like Qatar's 4.8% (approximately 30 basis points above the sovereign curve), reflect not merely opportunistic buying by PIMCO but a discreet admission that even states with among the world's largest sovereign wealth funds require rapid dollar liquidity when export receipts collapse.

This phenomenon fits a recurring pattern observed in prior stress episodes. During the 2014-2016 oil price crash, Saudi Arabia and other GCC members similarly increased bond issuance, yet largely through public markets. The current preference for private placements, as noted in the Bloomberg-compiled data totaling $13.8 billion regionally, minimizes disclosure requirements on reserve drawdowns and SWF liquidity positions. What the original coverage under-emphasized is the signal this sends about the limitations of economic diversification initiatives such as Saudi Vision 2030 and UAE Centennial 2071. Despite repeated official statements emphasizing reduced oil dependence, primary fiscal data continues to show hydrocarbon revenues comprising over 60% of budgets in most GCC states according to latest national statistical authorities.

The episode also illuminates the expanding role of non-bank financial intermediaries in sovereign financing during geopolitical shocks. BIS data on non-bank financial intermediation from its March 2025 Quarterly Review highlights that private credit assets under management globally exceeded $2.1 trillion, with dedicated emerging-market vehicles showing particular appetite for short-duration, high-quality sovereign exposure. PIMCO's opening of a Dubai office in 2024 and its stated long-term hold strategy position the firm as a quasi-lender of last resort, a role traditionally played by multilateral institutions or official swap lines. This development carries multiple interpretations: Gulf officials, including the UAE ambassador's recent statements to U.S. counterparts, frame these arrangements as routine portfolio management rather than distress signals. Meanwhile, credit analysts note that the premium paid for speed and confidentiality represents an implicit cost of opacity during wartime uncertainty.

U.S. Treasury Secretary Scott Bessent's confirmation of multiple Gulf requests for Federal Reserve swap lines, alongside President Trump's public comments on potential UAE arrangements, adds another layer. These parallel official channels suggest that private credit from PIMCO is not replacing but complementing potential public liquidity backstops. The original reporting correctly identifies the three borrowers as those with strongest balance sheets yet misses the broader implication: if even these states face dollar shortages amid conflict, smaller or more leveraged oil producers may encounter significantly higher borrowing costs or outright market exclusion. This dynamic elevates asset managers like PIMCO into de facto participants in geopolitical risk management, where capital allocation decisions influence which regimes maintain stability during energy supply shocks.

Synthesizing these threads, the PIMCO transactions reveal a hybrid financial architecture emerging in which non-bank credit providers fill gaps left by risk-averse public markets and politically constrained official institutions. Whether this represents prudent risk dispersion or defers necessary fiscal adjustments remains contested among economists. Primary documents, including the IMF staff reports and BIS locational banking statistics, suggest the former interpretation currently prevails, as default probabilities on GCC sovereign debt remain compressed. However, sustained geopolitical tension could test the sustainability of this private credit backstop, particularly if higher coupons begin to strain budgets already facing diversification spending pressures.

MERIDIAN: Even the GCC's strongest sovereign balance sheets are quietly paying premiums for rapid dollar liquidity via PIMCO as public markets freeze during conflict, signaling that private credit is becoming a parallel architecture for geopolitical risk absorption that official swap lines may soon reinforce.

Sources (3)

- [1]PIMCO Privately Lends Over $10 Billion To Dollar-Strapped Gulf States(https://www.zerohedge.com/geopolitical/pimco-privately-lends-over-10-billion-dollar-strapped-gulf-states)

- [2]IMF Middle East and Central Asia Regional Economic Outlook, April 2025(https://www.imf.org/en/Publications/REO/MECA/Issues/2025/04/15/regional-economic-outlook-middle-east-central-asia-april-2025)

- [3]BIS Quarterly Review, March 2025: Non-bank financial intermediation(https://www.bis.org/publ/qtrpdf/r_qt2503.htm)