Enduring Chokepoint Vulnerabilities: The Safeen Prestige Sinking and Systemic Risks to Global Energy Flows

Beyond the Safeen Prestige sinking, analysis reveals insurance-driven deterrence, historical Tanker War parallels, and a projected multi-month 12 Mb/d oil shortfall likely pushing Brent toward $130/bbl, synthesizing EIA chokepoint data, UNCLOS principles, and UBS traffic assessments while noting coverage gaps on systemic risk transmission.

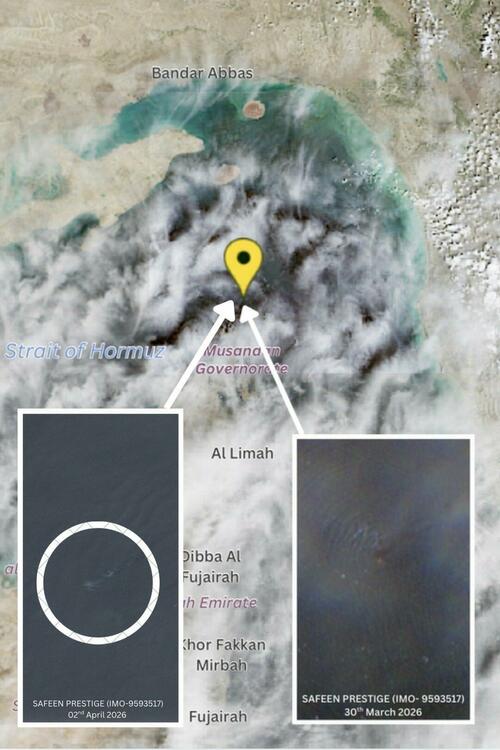

The confirmed sinking of the Maltese-flagged, Egyptian-owned container vessel Safeen Prestige (IMO 9593517) in the Strait of Hormuz, first damaged by an Iranian strike in early March 2026, extends beyond a single maritime casualty. Satellite imagery from the EU Copernicus programme and hydrographic data from Pakistan's National Hydrographic Office document the vessel's progressive disappearance, leaving only surface slicks. While the ZeroHedge report accurately relays Bloomberg-sourced details, UBS analyst updates, and ownership data from Sayari and TradeWinds, it underplays longer-term insurance market reactions and historical patterns of escalation.

Primary documentation from the 1980s Tanker War—UN Security Council Resolution 598 (1987) and contemporaneous IMO records on attacks on neutral shipping—reveals repeated use of mines, missiles, and selective interdiction against commercial traffic. Those incidents prompted reflagging operations, naval convoys, and eventual U.S. military engagement. Current events echo this pattern: the IRGC's reported continued ignition of the Safeen Prestige and statements permitting only 'friendly' or Iraqi vessels mirror earlier tactics of calibrated disruption rather than outright closure.

What initial coverage missed is the compounding effect on war-risk insurance. Lloyd's Joint War Committee has previously listed the Strait and surrounding waters as a Listed Area during periods of tension, driving premium surges of 500-1000% as seen after the 2019 tanker attacks. The present selective transit policy—two Qatari LNG carriers turning back, limited tanker exits, and no observable normalization despite weekend Iraqi exceptions—creates de facto deterrence for commercial operators even without a physical blockade. This raises delivered costs for all cargoes transiting the region.

Synthesizing EIA primary analysis of world oil chokepoints (which records roughly 21 million barrels per day of crude and products moving through Hormuz, equating to approximately one-fifth of global petroleum consumption) with UBS's latest estimate of a 12 Mb/d shortfall pre-SPR release underscores the scale. Iraqi production has already fallen more than 3 Mb/d due to constrained alternatives. Qatar LNG flows face similar friction. These figures align with observed Red Sea disruptions since late 2023, where Houthi actions, often linked to broader Iran-aligned strategies, forced rerouting around the Cape of Good Hope, adding 10-14 days and thousands of dollars per TEU.

Perspectives differ sharply. Iranian statements frame actions as legitimate responses within territorial waters and self-defense under Article 51 of the UN Charter. U.S. and allied primary releases emphasize freedom of navigation principles codified in UNCLOS Part III. Shipping associations, citing IMO circulars on maritime security, highlight crew safety and the risk of accidental escalation. Global importers such as China, India, and Japan—dependent on Gulf crude—face inflationary pressure without direct involvement in the U.S.-Iran standoff.

The combination of a sunk non-oil vessel, persistent shortfall, and elevated insurance premia points to a multi-month disruption scenario more consistent with UBS's $130/bbl Brent pathway than rapid normalization (Polymarket currently prices only 13% probability of normal traffic by end-April). Without sustained diplomatic de-escalation or expanded alternative export infrastructure, secondary effects on inflation, Asian LNG pricing, and global supply-chain costs will likely persist irrespective of short-term SPR deployments or deadline extensions.

MERIDIAN: Selective vessel targeting and transit permissions in the Strait of Hormuz signal calibrated pressure rather than total blockade, likely sustaining a 10-12 Mb/d shortfall and elevated insurance costs that keep Brent structurally higher through 2026 even if formal deadlines are extended.

Sources (3)

- [1]Primary Source(https://www.zerohedge.com/markets/container-ship-sinks-hormuz-after-iranian-strike-last-month-ubs-gives-latest-strait-update)

- [2]EIA World Oil Chokepoints(https://www.eia.gov/international/analysis/special-topics/World_Oil_Chokepoints)

- [3]UN Security Council Resolution 598(https://undocs.org/S/RES/598(1987))