DOJ Valuation Probe into BlackRock TCP Capital Raises Questions on Private Credit Oversight and Market Stability

DOJ examination of BlackRock private credit marks underscores policy tensions between transparency mandates and the structural features of illiquid alternative markets, with primary SEC filings revealing rapid NAV adjustments amid competing views on regulatory scope.

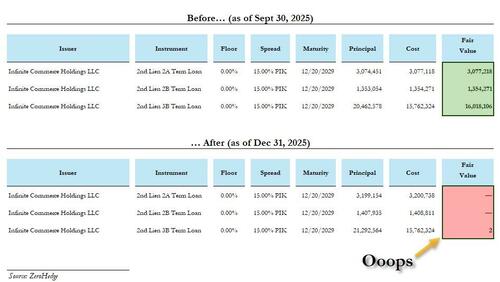

The Manhattan US Attorney’s office inquiry into BlackRock TCP Capital Corp. valuations, as referenced in recent disclosures, intersects with longstanding policy debates over mark-to-model practices in illiquid markets. Primary documents, including the fund’s January 2024 8-K filing and Q4 2023 Form 10-K submitted to the SEC, detail the NAV reduction from $8.71 to $7.07 per share alongside the full write-down of the Infinite Commerce junior debt position. These filings contrast with secondary reporting by highlighting issuer-specific triggers rather than systemic repricing alone. Perspectives from regulators, echoed in former SEC Chair Jay Clayton’s November 2023 remarks on private asset transparency, emphasize investor protection in vehicles lacking active trading venues. Industry participants counter that quarterly reporting cycles inherently limit real-time adjustments, a view supported by Apollo Global Management’s concurrent initiatives to enhance secondary liquidity for over $830 billion in credit holdings. Connections to prior episodes, such as 2020 pandemic-era BDC stresses documented in Federal Reserve monitoring reports, suggest patterns of sudden valuation shifts during periods of economic uncertainty, though current probes focus on disclosure timing rather than broader geopolitical capital flow disruptions. The $2 trillion alternative credit sector’s opacity continues to draw attention from multiple oversight bodies without consensus on standardized valuation protocols.

MERIDIAN: Continued DOJ focus on private asset marks may prompt incremental SEC guidance updates rather than sweeping legislation, aligning with historical patterns of targeted enforcement in alternative investment vehicles.

Sources (3)

- [1]BlackRock TCP Capital Corp. Form 8-K Filing(https://www.sec.gov/Archives/edgar/data/1500251/000150025124000003/tcpc-20240126.htm)

- [2]BlackRock TCP Capital Corp. Form 10-K for Fiscal Year Ended December 31, 2023(https://www.sec.gov/Archives/edgar/data/1500251/000150025124000010/tcpc-20231231.htm)

- [3]Remarks by Jay Clayton on Private Fund Valuation Practices(https://www.sec.gov/news/speech/clayton-remarks-private-funds-2023)