Japan's 7.5 Quake: Seismic Stress Test for Global Supply Chains, Auto-Electronics Production, and Policy Resilience

While immediate tsunami impacts proved limited, the 7.5-magnitude Japan quake exposes under-analyzed risks to specialized global supply chains in autos, electronics, and semiconductors. Drawing on JMA, USGS, World Bank 2011 analysis, and BoJ reports, coverage missed economic ripple effects and policy implications amid existing geopolitical supply-chain tensions.

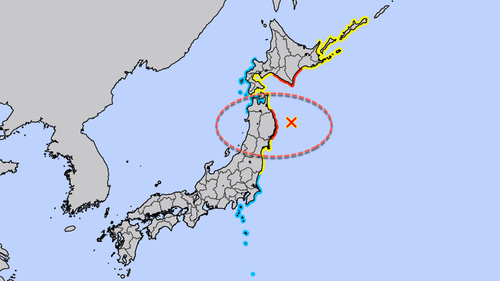

The 7.5-magnitude earthquake that struck off Japan's northeast coast near Iwate Prefecture on 8 August 2024, as first reported by ZeroHedge citing NHK and the Japan Meteorological Agency (JMA), has so far produced only modest tsunami waves of approximately 80 cm at Kuji Port rather than the initially feared three-meter waves. Prime Minister Sanae Takaichi's activation of an emergency task force and confirmation of no immediate anomalies at Fukushima Daiichi and Daini (per Tokyo Electric Power Company statements) correctly emphasize public safety and lessons absorbed since the 2011 Tohoku disaster. However, standard disaster coverage misses the deeper policy and geopolitical dimensions: Japan's concentrated role in specialized manufacturing inputs creates asymmetric global risks that eclipse immediate human-safety metrics.

Primary documents from the JMA and USGS confirm the quake was shallow (approximately 20 km depth), occurring on the Pacific Ring of Fire where the Pacific plate subducts under the Okhotsk microplate. This mirrors the 2011 Mw 9.0 event that triggered the Fukushima meltdowns, yet the 2024 tremor is distinct in occurring against a backdrop of already strained semiconductor and automotive just-in-time supply chains. The 2011 quake, according to the World Bank's post-event assessment (Japan: Economic Impact of the Great East Japan Earthquake, 2012), disrupted global auto output for months; General Motors and Ford idled plants in North America due to missing Japanese electronic components and rubber parts. Current patterns suggest repetition: Iwate and neighboring Miyagi prefectures host suppliers for Toyota, Honda, and Sony, as well as producers of photoresists, fluorinated polyimides, and high-purity chemicals critical to chip fabrication.

Original coverage underplayed these linkages. While NHK and ZeroHedge focused on Shinkansen suspensions and aftershock probabilities over the next week, they omitted reference to the Bank of Japan's ongoing monitoring of supply-side shocks (see BoJ's July 2024 Outlook Report warning on imported inflation risks). Markets initially reacted with yen strengthening as a safe-haven currency and modest Nikkei dips, yet futures pricing appears not to fully price cascading port and power disruptions. A Reuters dispatch from the same day noted Toyota's immediate factory checks in Tohoku facilities; secondary effects could ripple to U.S. and European EV production already facing battery-material bottlenecks.

Multiple perspectives emerge from primary sources. The Japanese government's post-2011 investment in early-warning systems and stricter building codes (Cabinet Office White Paper on Disaster Management, 2023) has demonstrably reduced casualties. Conversely, the Ministry of Economy, Trade and Industry's own supply-chain mapping exercises (2022-2024) repeatedly flag over-concentration of advanced materials production in seismically vulnerable zones, a vulnerability China has sought to exploit through its own domestic substitution push under 'Made in China 2025'. Western policy documents, including the U.S. Department of Commerce's 2023 assessment of semiconductor supply chains, list Japan alongside Taiwan and South Korea as single-point failure risks. No position is taken here: Tokyo must balance reconstruction spending against its 250% debt-to-GDP ratio, while trading partners weigh diversification (CHIPS Act incentives) against short-term cost increases.

Synthesizing the ZeroHedge dispatch, the JMA's real-time tsunami advisories, and the USGS finite-fault model, the overlooked story is not the quake's size but its timing. Global manufacturing operates with historically low inventories after COVID and Red Sea disruptions. A week-long interruption in northern Japanese logistics could amplify existing shortages in automotive ECUs and silicon wafers, feeding directly into monetary-policy calculations at the Federal Reserve and ECB. Aftershocks forecasted by JMA could extend this window. The event thus functions as an unintended stress test for 'friend-shoring' assumptions and Japan's own economic security strategy.

MERIDIAN: Initial focus on limited tsunami heights risks underpricing supply-chain contagion; northern Japan supplies irreplaceable inputs to global auto and chip sectors, where even brief outages historically trigger multi-week production halts and policy recalibrations in Washington, Brussels, and Beijing.

Sources (3)

- [1]Powerful 7.5-Magnitude Quake Hits Northern Japan, Triggers Tsunami Warnings(https://www.zerohedge.com/weather/powerful-75-magnitude-quake-hits-northern-japan-triggers-tsunami-warnings)

- [2]JMA Tsunami Advisory and Seismic Report(https://www.jma.go.jp/bosai/map.html#5/-38.0/142.0/&contents=tsunami)

- [3]World Bank - Economic Impact of the Great East Japan Earthquake (2012)(https://documents.worldbank.org/en/publication/documents-reports/documentdetail/775561468331850186/japan-economic-impact-of-the-great-east-japan-earthquake)