AI Drives 75% of US Q1 GDP Growth: A Structural Shift or Fragile Boom?

AI accounted for 75% of US Q1 GDP growth, signaling a structural economic shift but also exposing risks like supply chain vulnerabilities, consumer fragility, and regulatory gaps. This analysis goes beyond the headline to explore historical parallels, international dependencies, and policy challenges.

The latest US GDP report for Q1 reveals a striking statistic: approximately 75% of the 2.0% annualized growth was driven by Artificial Intelligence (AI)-related investments, particularly in nonresidential fixed investment sectors like software and information processing equipment. According to the Bureau of Economic Analysis (BEA), nonresidential fixed investment contributed 1.38% to the GDP growth, with software and data center equipment—key components of AI infrastructure—accounting for 1.5% of the total 2.0% increase. This unprecedented reliance on AI signals a potential structural shift in the US economy, but it also raises questions about sustainability and overlooked vulnerabilities that mainstream coverage, such as the ZeroHedge report, has not fully addressed.

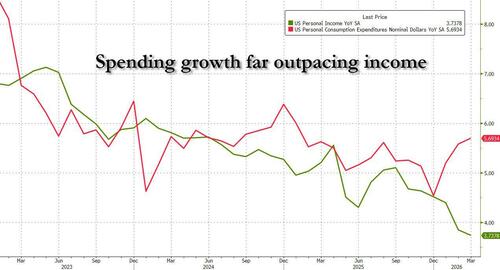

ZeroHedge's analysis focuses on the raw numbers, emphasizing AI's role in driving growth through software (0.7%) and equipment (0.88%). However, it misses critical context about the broader implications of this dependency. First, the report does not explore the concentration risk of such heavy reliance on a single sector. Historical patterns, such as the dot-com bubble of the late 1990s, suggest that overinvestment in a nascent technology can lead to severe corrections if growth expectations are not met. The BEA data also shows a decline in personal savings to a three-year low, alongside consumer spending growth (1.6%) outpacing income growth—a dynamic ZeroHedge attributes to temporary stimulus but does not connect to AI-driven economic distortions. If consumer spending weakens without a corresponding increase in other sectors, the economy’s dependence on AI investment could become a liability.

Second, the international dimension is underexplored. Net exports subtracted 1.3% from GDP growth, per the BEA, reflecting a surge in imports over exports. A significant portion of AI-related equipment, such as semiconductors and data center hardware, is imported, as highlighted in a 2023 report by the US International Trade Commission (USITC). This raises concerns about supply chain vulnerabilities, especially amid geopolitical tensions with key suppliers like China. For instance, restrictions on semiconductor exports to the US, as seen in recent US-China trade disputes, could disrupt the AI investment boom. ZeroHedge’s framing of AI as a 'core anchor' of the economy overlooks how external dependencies could undermine this pillar.

Finally, the policy angle deserves deeper scrutiny. ZeroHedge suggests the US government will inevitably backstop AI if a bubble bursts, but it does not consider how current policies are already shaping this trajectory. The CHIPS and Science Act of 2022, which allocates $52 billion to bolster domestic semiconductor production, indicates a proactive effort to reduce reliance on foreign supply chains. Yet, as the Congressional Research Service (CRS) notes, implementation lags and workforce shortages may delay these benefits, leaving the AI-driven growth vulnerable in the near term. Moreover, the lack of regulatory frameworks for AI development—despite calls for oversight in areas like data privacy and algorithmic bias—could amplify risks of market overconfidence, a factor absent from ZeroHedge’s narrative.

In synthesizing these perspectives, a pattern emerges: AI’s role in US economic growth is not merely a technological triumph but a double-edged sword. It reflects a structural pivot toward a digital economy, akin to the industrial shifts of the early 20th century, but it also mirrors speculative booms that have historically destabilized markets. The BEA data underscores AI’s dominance, while USITC and CRS reports highlight external and policy risks that could temper this momentum. Mainstream coverage often stops at the headline figure of 75%, missing the interplay of consumer fragility, global supply chains, and regulatory gaps. Whether this marks a lasting transformation or a fragile bubble depends on how these underlying tensions are managed—a question that will define the US economic landscape in the coming years.

MERIDIAN: The heavy reliance on AI for US GDP growth could face a stress test within the next 12-18 months if supply chain disruptions or consumer spending declines materialize, potentially forcing policymakers to accelerate domestic tech investments.

Sources (3)

- [1]Bureau of Economic Analysis: Q1 2025 GDP Report(https://www.bea.gov/news/2025/gross-domestic-product-first-quarter-2025-advance-estimate)

- [2]US International Trade Commission: Semiconductor Supply Chain Report 2023(https://www.usitc.gov/publications/332/pub5453)

- [3]Congressional Research Service: CHIPS and Science Act Implementation Update(https://crsreports.congress.gov/product/pdf/R/R47523)