Uranium Supply Crunch and SMR Surge Signal Overlooked Nuclear Revival

Structural uranium deficits projected to reach 32% by 2045, combined with reactor life extensions to 80 years, new builds across continents, and surging SMR development backed by DOE and military programs, indicate an accelerating nuclear revival that offers reliable baseload power largely sidelined in mainstream renewables-focused coverage.

While mainstream energy coverage continues to emphasize intermittent renewables, a confluence of reactor life extensions, new builds, and accelerating small modular reactor (SMR) development is exposing structural uranium supply deficits that could reshape global power generation. Goldman Sachs analyst Brian Lee has highlighted a widening uranium market imbalance, with the cumulative supply-demand gap now projected at 1.914 billion pounds through 2045—up significantly from prior estimates. This reflects updated assumptions around reactor lifespans extended to 80 years on average, accelerated new construction (including 20 new U.S. reactors and restarts), and rising demand that creates a 13% deficit through 2035 expanding to 32% by 2045. Spot prices are forecasted to reach $91 per pound by end-2026, representing 20% upside.[1][1]

Recent developments underscore this momentum. In the United States, the Nuclear Regulatory Commission completed its fastest-ever subsequent license renewal for Duke Energy’s Robinson Unit 2, extending operations to 80 years through 2050. Similar approvals for Florida Power & Light’s St. Lucie units secure output potentially to 2063. A Brookfield and The Nuclear Company joint venture is advancing due diligence on completing the long-stalled VC Summer AP1000 units in South Carolina. These moves align with broader federal efforts to streamline nuclear expansion.[2]

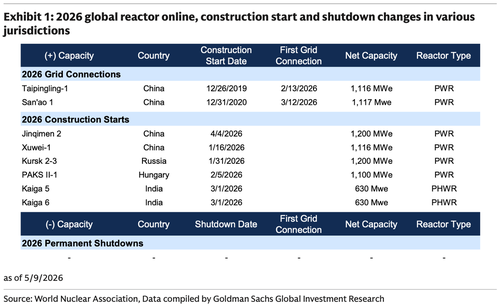

Canada’s Bruce Power signed an MoU with SaskPower to share expertise on large reactors as Saskatchewan advances both conventional and SMR programs. In Europe, Czech utility ČEZ is preparing 80-year life extensions for Dukovany reactors, Belgium is negotiating state takeover of its full nuclear fleet to preserve life-extension options, and Bulgaria is pushing fixed-price contracts for new Kozloduy AP1000 units to control costs. Asia continues apace: South Korea’s Saeul Unit 3 reached criticality, Japan restarted Kashiwazaki-Kariwa 6 (the first TEPCO reactor back online since Fukushima), India’s NTPC and EDF signed an MoU exploring EPR technology deployment, and Kazakhstan adopted a strategy for at least three nuclear plants by 2050 with SMR assessment. Lithuania advanced Ignalina decommissioning while these new capacity additions proceed.[3]

SMRs represent a critical connection others often miss. By enabling factory fabrication, lower upfront capital, siting flexibility, and applications beyond traditional grids—including data centers, industrial heat, remote communities, and microgrids—SMRs lower barriers that have stalled large-reactor builds for decades. The U.S. Department of Energy has committed $900 million in funding, launched pilot programs for advanced reactor testing, and supported military microreactor deployments at bases. Over 70 SMR designs are in development globally according to IAEA tracking, with designs spanning light-water, gas-cooled, molten-salt, and sodium-cooled technologies. Many incorporate high-assay low-enriched uranium (HALEU) for improved efficiency, though this creates new fuel supply chain demands. EIA analysis notes SMRs and microreactors could address the 98 GW U.S. nuclear fleet’s limited recent growth by offering scalable, reliable baseload that intermittent wind and solar cannot match without massive storage.[4][4]

World Nuclear Association and NEI reporting confirm private investment, regulatory streamlining (including NRC proposals for faster microreactor licensing), and state-level policies are accelerating this shift. The nuclear revival is not merely additive to renewables but foundational: high capacity factors near 90% provide the firm power essential for electrifying industry, supporting AI infrastructure, and maintaining grid stability as variable sources grow. Uranium’s structural deficit—exacerbated by mine supply lags, geopolitical restrictions on Russian supply, and secondary sources drying up—suggests prices and project momentum will continue climbing even as media narratives favor solar and wind subsidies. This quiet renaissance, backed by life extensions adding decades of output and SMRs unlocking new markets, points to nuclear’s expanding role in energy security through 2050.

Energy Analyst: Widening uranium deficits and SMR policy tailwinds will likely sustain higher nuclear fuel prices and drive faster deployment of reliable baseload capacity, exposing the limits of intermittency-focused energy strategies.

Sources (5)

- [1]Supply Gap Signals Sustained Rise in Uranium Prices, Goldman Sachs Bullish Until 2026(https://nai500.com/blog/2025/12/supply-gap-signals-sustained-rise-in-uranium-prices-goldman-sachs-bullish-until-2026/)

- [2]Small modular reactors and microreactors under development in the United States(https://www.eia.gov/todayinenergy/detail.php?id=67584)

- [3]NRC Completes Fastest-Ever Reactor License Renewal, Extending Operations To 2050(https://www.nrc.gov/sites/default/files/cdn/doc-collection-news/2026/26-046.pdf)

- [4]Small Modular Reactors(https://world-nuclear.org/information-library/nuclear-power-reactors/small-modular-reactors/small-modular-reactors)

- [5]State of the Nuclear Industry 2026 | NEI(https://www.nei.org/news/state-of-the-nuclear-industry-2026)