AI's Hidden Grid Crisis: Texas Demand Quadruple Projection Exposes Structural Energy Bottlenecks Beyond ERCOT's Own Caveats

ERCOT's explosive demand forecast reveals AI-driven data center growth creating unprecedented strain on U.S. energy infrastructure. Analysis uncovers operator skepticism, missed distinctions between load types, transmission limits, and broader geopolitical implications missed by initial coverage.

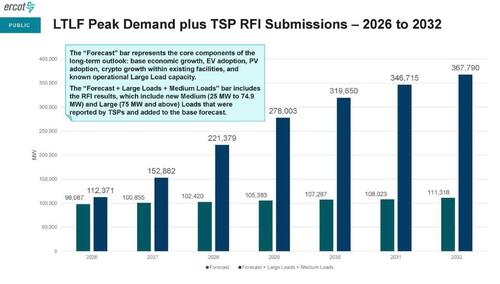

The Electric Reliability Council of Texas (ERCOT) preliminary long-term load forecast released this week projects peak demand soaring to 367,790 MW by 2032 — more than four times the August 2023 record of 85,508 MW. While initial coverage focused on the headline shock value, it missed critical nuances in ERCOT's own accompanying caveats, the distinction between AI-specific loads versus crypto and industrial demand, and the deeper pattern of hyperscale computing now colliding with U.S. grid planning realities.

Primary documents reveal ERCOT leadership is actively distancing itself from the raw numbers. In formal comments to the Public Utility Commission of Texas (PUCT), Senior Vice President Chad Seely stated the operator 'has concerns with using the preliminary load forecast values for the Reliability Assessment and any other transmission and resource adequacy analysis,' signaling intent to seek adjustments. ERCOT President and CEO Pablo Vegas added that 'this forecast [is] higher than expected future load growth' due to evolving methods of identifying and verifying large loads under Senate Bill 6, passed last year to force better utility reporting on data centers and similar customers.

This skepticism matters. The forecast aggregates utility-provided data on data centers, cryptocurrency mining, oil-and-gas processes, and manufacturing. Yet the AI component — driven by training and inference clusters for large language models — follows a different trajectory than Bitcoin mining, which proved more flexible and mobile during prior ERCOT stress periods such as Winter Storm Uri in 2021. Coverage largely collapsed these categories, underplaying how hyperscalers (Microsoft, Google, Amazon, Oracle) are signing long-term, high-capacity-factor contracts that function as near-baseload demand.

Synthesizing ERCOT's filing with the IEA's Electricity 2024 report and Goldman Sachs' April 2024 analysis illuminates the gap. The IEA documents that global data center electricity consumption is on track to double by 2026, with AI acceleration as the primary driver. Goldman Sachs separately estimates data centers could represent up to 8% of U.S. power demand by 2030, up from 3% today, with AI-related power needs growing faster than overall sector forecasts. Neither document was referenced in original reporting.

What existing coverage missed is the transmission bottleneck layered atop generation shortfall. Even if new gas-fired capacity is permitted rapidly under Texas's deregulated model, the interconnection queue for large loads now exceeds 100 GW, with multi-year delays for substations and high-voltage lines. This mirrors documented strains in Northern Virginia's 'Data Center Alley' (Dominion Energy's repeated warnings of 30-50% load growth) and Ireland's de facto moratorium on new data centers due to grid saturation.

Multiple perspectives emerge from primary sources. Hyperscale operators argue AI delivers productivity gains justifying the load, citing economic impact studies submitted to the PUCT. Grid planners emphasize reliability risks, pointing to ERCOT's own summer 2026 peak projection of 90,500-98,000 MW — far below the long-term model's 112,000 MW inflection point. Environmental policy documents, including recent EPA and DOE filings, highlight tension with decarbonization targets if incremental demand is met primarily by combined-cycle gas rather than delayed nuclear or overbuilt renewables plus storage. Texas policymakers, via SB 6 and ongoing legislative debate, view the load growth as economic development requiring pragmatic supply expansion.

Markets are only beginning to internalize the duration and inelasticity of this shift. Forward power curves in ERCOT hubs have steepened, yet equity analysts continue modeling utility capex primarily around EVs and electrification rather than sustained AI capex cycles measured in gigawatts. The long-term implication is a potential re-pricing of 'always-on' generation assets — including advanced nuclear and firm renewables with storage — as optionality becomes strategically valuable in national AI competitiveness relative to constrained grids in Europe and Asia.

The ERCOT episode is thus less a Texas anomaly than an early indicator of structural strain: AI compute is transitioning from marginal to foundational infrastructure demand. Primary grid operator documents suggest the eventual realized growth may be revised downward, yet the directional multi-year trend remains intact and under-appreciated in current capital allocation.

MERIDIAN: ERCOT's own caution on its quadruple-demand forecast underscores how difficult it is to model AI-driven load growth, yet the sustained trajectory will compel utilities and markets to accelerate firm generation and transmission investments well before 2030 as compute becomes a primary driver of baseload electricity needs.

Sources (3)

- [1]Texas Electricity Demand Could Quadruple Due To Soaring Data Center Demand: ERCOT(https://www.zerohedge.com/energy/texas-electricity-demand-could-quadruple-due-soaring-data-center-demand-ercot)

- [2]Electricity 2024 - Analysis(https://www.iea.org/reports/electricity-2024)

- [3]AI is poised to drive 160% increase in data center power demand(https://www.goldmansachs.com/insights/articles/ai-poised-to-drive-160-increase-in-data-center-power-demand)