AI's Structural Power Demand: Data Centers Drive Half of US Electricity Growth, Reshaping Utility Policy and Energy Security

IEA data confirms data centers drove half of 2025 US electricity demand growth amid AI expansion. Analysis links this to EIA projections, NERC reliability assessments, and DOE grid studies, revealing underreported permanence of load, geopolitical competition with China, divergent stakeholder perspectives on utilities vs. decarbonization, and policy implications for infrastructure and the energy transition.

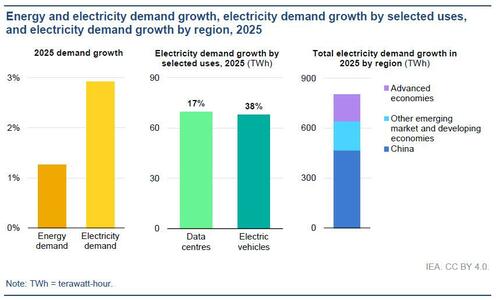

The IEA's Global Energy Review documents a 2% rise in US electricity demand in 2025, with data centers alone accounting for roughly half of that incremental load and the buildings sector driving 80% of total growth. This figure, highlighted in ZeroHedge's coverage, aligns with primary data from the US Energy Information Administration's Electric Power Monthly reports showing hyperscale facilities concentrated in PJM, ERCOT, and Virginia-dominant zones. However, mainstream reporting frequently frames this as a generic "data center" story, underplaying the direct link to AI model training and inference workloads that exhibit far less elasticity than traditional computing.

Synthesizing the IEA primary release with the EIA's Annual Energy Outlook 2025 reference case and the Department of Energy's "Assessing the Electric Grid's Readiness for AI" technical memorandum reveals patterns missed in initial coverage. EIA projections indicate data center demand could double to 9-12% of national electricity by 2030 under current AI deployment trajectories, a structural baseline load unlike weather-driven peaks or even EV charging curves. The IEA simultaneously records global solar additions of 600 TWh and record battery storage deployments, yet US-specific NERC 2025 Long-Term Reliability Assessment documents interconnection queues exceeding 2 TW, with data center projects facing multi-year delays due to transmission constraints.

Geopolitical context further complicates the picture. China's energy intensity rebound to over 3% improvement in 2025, per IEA data, coincides with its parallel expansion of AI-related semiconductor fabs and hyperscale clusters, underscoring a great-power competition where energy abundance becomes a strategic input. US policy documents, including draft FERC Order 1920 follow-ons on transmission cost allocation, reflect tension between states seeking rapid generation additions and federal emphasis on decarbonization via the Inflation Reduction Act's tax credits.

Multiple perspectives emerge from primary sources. Utility earnings calls and SEC filings from Dominion, Constellation, and Vistra portray the demand surge as credit-positive, justifying accelerated capital expenditure on combined-cycle gas, nuclear restarts, and small modular reactor licensing. Environmental NGOs citing EPA modeling argue that absent parallel acceleration of renewables and storage, this load risks prolonging fossil dependence and delaying national 2035 clean electricity targets. Grid operators in ISO/RTO dockets emphasize reliability risks, pointing to winter heating degree day spikes noted by IEA that coincided with data center baseload to stress test reserve margins.

What original coverage underplayed is the permanence: AI-driven demand is not cyclical but compounds with each new model generation, creating policy pressure for "all-of-the-above" approaches that challenge narratives favoring variable renewables alone. Lawrence Berkeley National Lab efficiency studies cited in DOE memoranda show compute energy intensity improving, yet absolute demand outpaces gains. This dynamic forces reevaluation of energy transition timelines, infrastructure permitting reform bills before Congress, and potential revisions to national security directives linking AI superiority to domestic power capacity. The IEA's own conclusion on electrification accelerating faster than total energy growth signals that data centers are not an isolated sector story but a bellwether for how technology, geopolitics, and energy policy increasingly converge.

MERIDIAN: Data center driven electricity growth is forcing US policymakers to reconcile AI technological competition with China against grid reliability and decarbonization targets, likely accelerating nuclear permitting and transmission reform over the next 24 months.

Sources (3)

- [1]IEA Global Energy Review(https://www.iea.org/reports/global-energy-review-2026)

- [2]EIA Annual Energy Outlook 2025(https://www.eia.gov/outlooks/aeo/)

- [3]DOE Assessing the Electric Grid's Readiness for AI(https://www.energy.gov/policy/articles/assessing-electric-grids-readiness-ai)