US Manufacturing Resilience Defies Geopolitical Volatility as Core Durable Goods Orders Rise for 11th Straight Month

Eleven consecutive months of core durable goods orders growth highlight sustained U.S. manufacturing demand and policy-driven industrial revival. The analysis connects this trend to CHIPS Act and IRA investments, contrasts it with recession forecasts, and notes what volatile-headline-focused coverage missed: structural friend-shoring gains and strategic economic positioning amid Ukraine war and U.S.-China tensions. Multiple perspectives from primary government data and institutional reports are presented without endorsement.

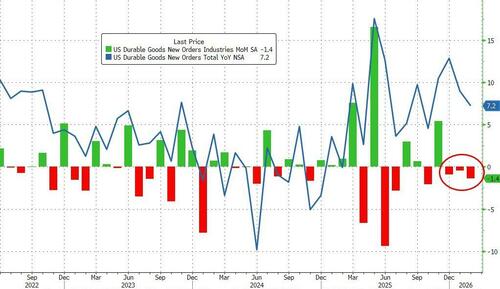

The U.S. Census Bureau's Advance Report on Durable Goods Manufacturers' Shipments, Inventories and Orders for February 2024 reveals core orders (excluding transportation) rose 0.8% month-over-month, marking the 11th consecutive monthly gain and lifting year-over-year growth to 5.97%—the strongest since August 2022. While the headline figure declined 1.4% due to civilian aircraft volatility, shipments—which feed directly into GDP—rose 0.9%, outpacing expectations. This sustained strength in non-defense capital goods orders (up 0.6%) signals persistent business investment and demand resilience.

The original ZeroHedge coverage accurately flags the mixed headline print and references possible war impacts on capital goods but misses the deeper structural context. It underemphasizes how this trend connects to deliberate U.S. industrial policy. Primary documents from the Department of Commerce and the White House fact sheets on the CHIPS and Science Act and Inflation Reduction Act document over $400 billion in announced private-sector investments in semiconductors, clean energy, and advanced manufacturing since 2022. These policies are channeling demand into domestic production, a pattern also visible in the Federal Reserve's industrial production data and the ISM Manufacturing New Orders index, which has remained in expansion territory despite broader survey softness.

This data challenges the dominant 2023 recession narrative advanced by several major banks and some Federal Reserve officials. Where coverage focused on short-term volatility and aircraft orders from Boeing, it overlooked the broader decoupling and "friend-shoring" dynamic: U.S. manufacturers have diversified away from vulnerable global supply chains strained by the Russia-Ukraine conflict, Red Sea disruptions, and U.S.-China technology restrictions. Cross-referencing the Census Bureau release with the IMF's April 2024 World Economic Outlook shows the U.S. manufacturing sector outperforming Eurozone counterparts still grappling with energy shocks from the Ukraine war.

Multiple perspectives emerge. Administration analyses cite these figures as evidence that targeted fiscal policy has achieved a soft landing, reinforcing domestic industrial capacity while navigating geopolitical headwinds. Skeptical voices, including analyses from the Congressional Budget Office on long-term debt sustainability, counter that elevated federal spending and deficits are artificially supporting demand and that higher-for-longer interest rates may yet trigger a sharper slowdown in capital expenditure. Geopolitical analysts note that manufacturing strength enhances U.S. leverage in trade negotiations and technology export controls, reducing economic coercion risks from strategic competitors.

What others missed is the policy-to-data transmission mechanism: the 11-month streak aligns with accelerated implementation timelines of the IRA and CHIPS Act, suggesting a structural rather than purely cyclical rebound. This resilience contrasts with persistent market jitters over election uncertainty, Middle East escalation risks, and potential retaliatory tariffs. The data does not eliminate vulnerabilities—particularly inventory swings or lagged effects of monetary tightening—but it complicates easy recession calls and invites policymakers to reassess assumptions about economic fragility amid great-power competition. Synthesis of the Census Bureau primary release, ISM reports, and Commerce Department investment tallies paints a more nuanced portrait: U.S. manufacturing is exhibiting durable underlying momentum that geopolitical turbulence has not yet eroded.

MERIDIAN: Sustained core durable goods growth reveals structural manufacturing revival tied to domestic industrial policy that persists beneath geopolitical market volatility, likely forcing both the Fed and Congress to adjust recession assumptions and trade strategy.

Sources (3)

- [1]U.S. Census Bureau - Advance Report on Durable Goods Manufacturers' Shipments, Inventories and Orders(https://www.census.gov/econ/currentdata/)

- [2]Institute for Supply Management - Manufacturing PMI Report(https://www.ismworld.org/supply-management-news-and-reports/reports/)

- [3]White House Fact Sheet: CHIPS and Science Act Implementation(https://www.whitehouse.gov/briefing-room/)