Starwood's Redemption Gate Exposes Deeper Cracks in Commercial Real Estate Amid Rising Rates

Starwood Capital Group’s gating of redemptions in its $22 billion real estate fund signals deeper vulnerabilities in the commercial real estate sector amid high interest rates. Beyond liquidity pressures, this move reflects systemic risks of declining valuations, over-leverage, and potential contagion across financial markets, drawing parallels to pre-2008 dynamics and highlighting underexplored economic headwinds.

Starwood Capital Group's decision to halt redemptions in its $22 billion Starwood Real Estate Income Trust (SREIT), as reported by Bloomberg and ZeroHedge, is not merely a reaction to elevated redemption requests but a signal of systemic vulnerabilities in the commercial real estate (CRE) sector under the weight of sustained high interest rates. While Starwood CEO Barry Sternlicht attributes the move to external pressures like interest rate spikes since 2022, this action underscores broader, underexplored risks of contagion across real estate funds and related financial markets that mainstream coverage often overlooks.

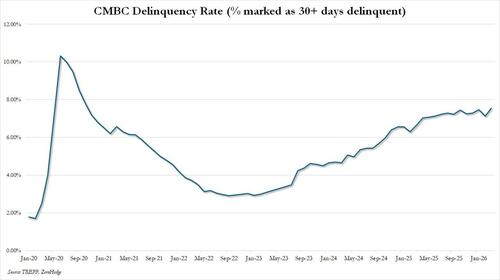

The CRE sector has been grappling with a deteriorating environment, as evidenced by the TREPP CMBS monthly report for March, which recorded a delinquency rate surge to 7.55%, the highest in years, driven by unexpected stress in lodging properties. Starwood's fund, heavily invested in 598 U.S. properties, mirrors this trend, with its cut in annualized distribution from 6.3% to 4.7% for Class I shares reflecting not just liquidity constraints but also a reassessment of asset valuations in a high-rate regime. What the original coverage misses is the historical parallel to the 2008 financial crisis, where real estate over-leverage and liquidity freezes in funds precipitated wider market turmoil. Starwood’s prior restriction of liquidity rights by over 80% two years ago, as noted by the Financial Times, suggests a pattern of defensive measures that could indicate deeper balance sheet issues than publicly acknowledged.

Beyond Starwood, the CRE sector’s challenges tie into a larger pattern of financial stress amplified by the Federal Reserve’s aggressive rate hikes since 2022. Higher borrowing costs have not only depressed property valuations but also strained leveraged investors and funds reliant on cheap debt—a dynamic insufficiently highlighted in the initial reporting. The International Monetary Fund’s (IMF) 2023 Global Financial Stability Report warns of 'significant downside risks' in CRE due to tighter financial conditions, noting that non-bank financial institutions like real estate funds are particularly exposed to sudden redemption waves. This context suggests Starwood’s move is less an isolated event and more a canary in the coal mine for similar funds, including those managed by peers like Blackstone and KKR, which also target retail investors.

Another overlooked angle is the potential for contagion beyond CRE funds into the broader financial system. The 2020 CARES Act-era liquidity injections masked underlying weaknesses in CRE by propping up valuations through low rates and forbearance programs. As these supports wane, funds like SREIT, which launched in 2018 during a low-rate boom, face a reckoning. The failed bid by hedge fund Saba Capital to buy 5% of SREIT shares at a steep discount, as reported by the Financial Times, hints at market skepticism about the fund’s stated net asset value—a red flag for investor confidence that could ripple to other funds if redemptions remain gated.

Starwood’s optimistic outlook, with Sternlicht citing expectations of lower rates under a potential new Fed Chair and geopolitical stabilization, appears speculative against current data. The U.S. Bureau of Economic Analysis reported a slowdown in GDP growth to 1.6% in Q1 2024, signaling economic headwinds that could further pressure CRE demand, particularly in office and retail segments already hit by remote work trends and e-commerce shifts. This economic backdrop, combined with CRE’s high debt maturity wall in 2024-2025 (as per IMF estimates), suggests that Starwood’s 'temporary' gate may extend longer than anticipated, risking investor trust and potentially triggering forced asset sales at distressed prices.

In synthesizing these perspectives, Starwood’s redemption gate is not just a tactical retreat but a manifestation of structural fragilities in CRE amplified by monetary policy shifts. The original coverage frames this as a liquidity issue tied to interest rates, but the deeper story lies in the interplay of over-leverage, declining valuations, and systemic risk—issues that could cascade if other funds follow suit. While Sternlicht emphasizes alignment with investors through Starwood’s $500 million stake in SREIT, the lack of transparency on asset quality and the reliance on credit facilities for past redemptions (per Financial Times) raises questions about whether such alignment can withstand prolonged market stress.

MERIDIAN: Starwood’s redemption gate may signal the start of broader distress in commercial real estate funds, with potential forced asset sales in 2024-2025 if high rates persist, exacerbating financial contagion risks.

Sources (3)

- [1]Sternlicht's Starwood Real Estate Fund Gates Redemptions(https://www.zerohedge.com/markets/sternlichts-starwood-real-estate-fund-gates-redemptions)

- [2]IMF Global Financial Stability Report 2023(https://www.imf.org/en/Publications/GFSR/Issues/2023/04/11/global-financial-stability-report-april-2023)

- [3]Starwood Taps Credit Line to Fund Withdrawals(https://www.ft.com/content/starwood-taps-credit-line-to-fund-withdrawals-2022)