Private Credit's Shadow Expansion: Subprime Parallels and Underplayed Systemic Risks

Examining private credit's rapid growth through the lens of subprime vulnerabilities, this analysis highlights opacity, liquidity mismatches, and interconnections that mainstream coverage underplays while presenting regulatory and industry perspectives from IMF, FSB, and Goldman sources.

Recent warnings from Goldman Sachs CEO David Solomon and former CEO Lloyd Blankfein have spotlighted stress in private credit markets, prompting comparisons to the 2008 financial crisis. The sourced ZeroHedge article via RealInvestmentAdvice.com reviews historical warnings, differentiates private credit from subprime mortgages, and references Goldman research suggesting limited macroeconomic spillovers. However, this coverage underplays the scale of opacity and interconnections that primary regulatory assessments have flagged.

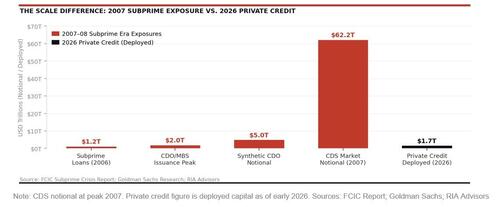

Private credit assets under management have grown from under $300 billion in 2010 to over $1.7 trillion by 2023, per Preqin data, fueled by post-GFC regulations that shifted lending from banks to non-bank entities. Unlike the originate-to-distribute model central to subprime, many private credit lenders retain exposure, yet the original analysis misses how redemption pressures in open-end funds create liquidity mismatches similar to those seen in other shadow banking episodes.

Synthesizing the IMF's April 2024 Global Financial Stability Report and the Financial Stability Board's 2023 Global Monitoring Report on Non-Bank Financial Intermediation reveals patterns overlooked in mainstream reporting. The IMF document highlights how private credit's involvement in leveraged finance can amplify downturns through correlated exposures with private equity. The FSB primary report documents increased non-bank intermediation risks, noting that insurers and pension funds hold substantial private credit positions, creating transmission channels to the real economy not fully captured in the sourced piece.

The 2008 crisis, as detailed in the Financial Crisis Inquiry Commission Report, stemmed from misaligned incentives, flawed ratings, and derivatives layering that multiplied exposure. Private credit differs in lacking the same synthetic CDO proliferation, yet echoes exist in underwriting standards under competitive pressure and limited transparency. What the original coverage got wrong was framing the debate as primarily 'contained credit cycle' versus 'full subprime repeat,' ignoring policy-induced growth: ultra-low rates post-2008 and Dodd-Frank's bank constraints deliberately expanded this shadow sector.

Multiple perspectives emerge from primary sources. Goldman Sachs' own shareholder letter acknowledges risks while its research arm downplays spillovers. Industry voices emphasize superior due diligence and higher covenants compared to 2006-era NINJA loans. Conversely, analyses from Soros fund leadership and Bank of England financial stability updates warn of potential fire sales and credit contraction impacting mid-market firms, which constitute the bulk of private credit borrowers.

This growth in the shadows, while providing capital where banks retreated, carries underappreciated systemic potential through indirect bank linkages via credit lines and collateral. Without taking a position, the evidence from regulatory primary documents suggests monitoring for amplification effects remains essential as interest rates remain elevated.

MERIDIAN: Private credit's expansion outside traditional regulation echoes past crisis patterns in opacity and leverage, yet structural differences may limit spillovers; policy responses will determine if risks remain contained.

Sources (3)

- [1]Subprime Crisis 2.0: Will Private Credit Be The Trigger?(https://www.zerohedge.com/markets/subprime-crisis-20-will-private-credit-be-trigger)

- [2]Global Financial Stability Report April 2024(https://www.imf.org/en/Publications/GFSR/Issues/2024/04/16/global-financial-stability-report-april-2024)

- [3]FSB Global Monitoring Report on Non-Bank Financial Intermediation 2023(https://www.fsb.org/2023/12/global-monitoring-report-on-non-bank-financial-intermediation-2023/)