IMF Flags Treasury Repricing Risks as US Debt Dynamics Intersect with Geopolitical Pressures

The IMF identifies erosion of the US Treasury safety premium and heightened rollover risks from short-term debt concentration as factors that could spark sudden yield repricing with worldwide liquidity consequences, especially when layered with geopolitical fiscal shocks.

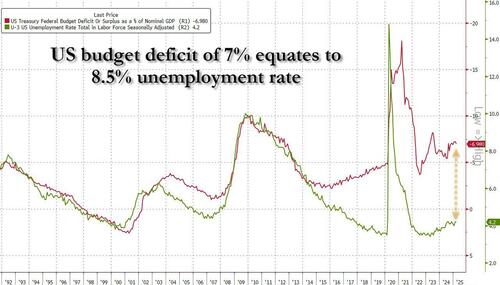

The IMF's April 2025 Fiscal Monitor explicitly warns that sustained US deficits averaging 6% of GDP, combined with elevated short-term bill issuance, are eroding the safety and liquidity premium of Treasuries. Primary data in the report shows AAA corporate spreads narrowing from over 55 basis points in early 2019 to approximately 35 basis points, a metric the IMF interprets as declining willingness of investors to pay extra for US government securities relative to high-grade corporates. This observation aligns with patterns seen in the Congressional Budget Office's 2024 Long-Term Budget Outlook, which projects federal debt held by the public reaching 122 percent of GDP by 2034 and continuing to climb absent policy changes.

Original coverage from ZeroHedge correctly highlights Treasury Secretary Scott Bessent's continuation of short-dated issuance because bill yields remain below longer-term coupons, yet it understates the historical context and global transmission channels. The IMF document itself references the increasing role of leveraged hedge funds in cash-futures basis trades, noting that liquidity supplied by these positions 'can be prone to flight' during volatility spikes, a vulnerability documented in the Federal Reserve's 2020 'Financial Stability Report' following the March dash-for-cash episode when even on-the-run Treasuries experienced severe dislocations. What coverage missed is the feedback loop between geopolitical shocks and fiscal rollover risk: the same IMF report ties Middle East tensions, including Iran-related conflicts, to new energy cost pressures that force governments to choose between fiscal support and debt restraint, amplifying US borrowing needs already elevated by prior emergency spending.

Synthesizing the IMF Fiscal Monitor, CBO projections, and the US Treasury's February 2025 Quarterly Refunding Announcement—which confirmed continued heavy bill issuance—the picture reveals a maturity profile shift unseen outside wartime. Average debt maturity has shortened, requiring more frequent refinancing at scales exceeding $1 trillion quarterly. This exposes the market to sudden sentiment shifts, as the IMF notes: 'If investors grow concerned about a country's rollover capacity, they may demand higher yields or step back from auctions.'

Multiple perspectives emerge from primary sources. US Treasury statements emphasize the unparalleled depth and liquidity of its market, arguing that foreign official holdings (per TIC data) and domestic demand remain robust. The IMF adopts a cautionary stance focused on cross-border spillovers, warning that higher US yields would raise borrowing costs globally, particularly for emerging markets with dollar-denominated debt. Meanwhile, recent BRICS communiques and People's Bank of China reserve diversification reports reflect a view that persistent US fiscal expansion accelerates de-dollarization trends, potentially reducing the buyer base for future issuance.

These elements point to a systemic vulnerability where a geopolitical trigger or volatility spike could precipitate global yield spikes and liquidity crises. The dynamics are self-reinforcing: rising interest costs (already surpassing defense outlays per CBO figures) generate political pressure that markets may price in advance, further elevating term premia. Unlike previous episodes confined to domestic policy normalization, current conditions intersect with elevated global fragmentation, making transmission faster and harder to contain through conventional central bank tools.

MERIDIAN: US fiscal trajectory and short-maturity concentration create conditions where an external shock like energy price spikes from conflict could force rapid global yield adjustments, compelling coordinated central bank liquidity provision while accelerating reserve diversification away from Treasuries.

Sources (3)

- [1]IMF Fiscal Monitor April 2025(https://www.imf.org/en/Publications/FM/Issues/2025/04/09/fiscal-monitor-april-2025)

- [2]Congressional Budget Office 2024 Long-Term Budget Outlook(https://www.cbo.gov/publication/59711)

- [3]U.S. Treasury Quarterly Refunding Announcement February 2025(https://home.treasury.gov/policy-issues/financing-the-government/quarterly-refunding/most-recent-quarterly-refunding-documents)