The Orbital Economy: Defense Convergence, Golden Dome, and the Multi-Trillion Structural Shift Beyond SpaceX's IPO

SpaceX IPO catalyzes visibility into a $600B+ space economy projected to reach $1.8T by 2035, with U.S. defense initiatives like Golden Dome driving budget surges, satellite infrastructure buildout, and intensifying U.S.-China rivalry—marking deeper capital reallocation and tech-defense convergence than surface-level coverage suggests.

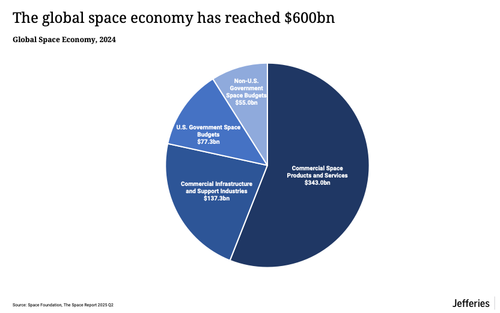

While mainstream coverage frames SpaceX's heavily oversubscribed IPO as a milestone for Elon Musk's empire and private spaceflight, deeper analysis reveals it as a pivotal marker in a broader reconfiguration of global capital flows toward orbital infrastructure, satellite constellations, and defense-tech integration that could redefine economic and strategic power through the 2030s. Corroborating data from independent research shows the global space economy has already surpassed $600 billion, with credible projections indicating growth to approximately $1.8 trillion by 2035, driven by both commercial applications and accelerating government investment, particularly in defense.

McKinsey's analysis in partnership with the World Economic Forum estimates the sector expanding from roughly $630 billion in 2023 to $1.8 trillion by 2035, encompassing 'backbone' infrastructure like satellites, launch services, and GPS alongside 'reach' applications that embed space tech into terrestrial industries from agriculture to autonomous vehicles. The Space Foundation's 2025 reporting confirms the economy hit a record $613 billion, projecting it could cross the $1 trillion threshold as early as 2032, fueled by commercial satellite broadband, Earth observation monetized via AI, and national security priorities.

A critical connection often missed in isolated tech reporting is the outsized role of defense spending. U.S. Space Force budgets have seen dramatic surges tied directly to the Golden Dome program—a multi-layered missile defense architecture integrating space-based sensors, interceptors, and AI command systems to counter ballistic, hypersonic, and cruise missile threats. Recent fiscal analyses document roughly 40% budget growth, with Space Force and related Missile Defense Agency allocations approaching $50 billion annually, eclipsing NASA's budget and signaling a strategic pivot where space is treated as warfighting domain rather than pure exploration. This program, with estimated costs ranging from $175-185 billion initially (and potentially far higher per independent assessments), has driven contracts to multiple firms for space-based interceptors, creating structural demand that benefits incumbents like SpaceX while spilling over into broader supply chains for satellite manufacturing and data infrastructure.

The U.S. maintains dominance, accounting for approximately 60% of global government space expenditure—around $80 billion versus China's nominal $20 billion (with PPP adjustments narrowing the effective gap). This rivalry extends to lunar ambitions: U.S. Artemis Accords now boast dozens of international partners targeting crewed landings by 2028 and outposts by 2030, contrasting with the smaller China-Russia coalition. Both nations have codified space as a strategic priority in national plans, underscoring how orbital assets are becoming foundational to future compute, communications, and resource economies—including potential low-Earth orbit data centers that reduce latency for AI and edge computing.

SpaceX's entrenched position as NASA's top commercial partner and its role across launches, comms, and national security data layers illustrates the deep public-private fusion. Rather than isolated success, the IPO reflects maturing capital markets recognizing space as a multi-decade tailwind where defense outlays catalyze commercial scale, potentially redirecting trillions in investment away from traditional terrestrial infrastructure toward resilient, dual-use satellite networks. This convergence—commercial broadband enabling global connectivity, defense sensors feeding AI systems, and lunar programs scouting resources—represents a structural economic reordering that mainstream outlets under-analyze amid quarterly earnings hype. By 2035, these shifts could underpin everything from hypersonic defense superiority to orbital manufacturing, positioning participants at the center of the next industrial epoch.

LIMINAL: Multi-trillion capital flows into orbital infrastructure and dual-use defense systems will quietly redefine 2030s economic architecture, turning low-Earth orbit into the indispensable backbone for AI, global connectivity, and strategic superiority far beyond headline IPO valuations.

Sources (5)

- [1]Space: The $1.8 trillion opportunity for global economic growth(https://www.mckinsey.com/industries/aerospace-and-defense/our-insights/space-the-1-point-8-trillion-dollar-opportunity-for-global-economic-growth)

- [2]The Space Report 2025 Q2 Highlights Record $613 Billion(https://www.spacefoundation.org/2025/07/22/the-space-report-2025-q2/)

- [3]Space Force names 12 companies to develop Golden Dome(https://defensescoop.com/2026/04/24/golden-dome-space-based-interceptor-missile-defense-contractors/)

- [4]FY 2026 Defense Space Budget: Emergence of Golden Dome(https://csps.aerospace.org/papers/fy-2026-defense-space-budget-emergence-golden-dome)

- [5]Defense Primer: The Golden Dome for America(https://www.congress.gov/crs-product/IF13115)