Blue Owl Redemption Surge: Liquidity Strains or Sentiment-Driven Stress in the $1.8 Trillion Private Credit Market?

Blue Owl's gating of redemptions after 41% demand in its technology income fund highlights liquidity mechanics in private credit. Analysis draws on firm letters, Goldman and Barclays research to show concentrated requests, standard fund safeguards, and differing views on systemic risk versus sentiment-driven pressure.

Blue Owl's announcement that it will cap redemptions at 5% for its OCIC and OTIC funds after quarterly requests reached 21.9% and 40.7% respectively marks a notable development in private credit. According to the firm's own investor letters, 90% of OCIC shareholders opted not to tender, indicating concentrated institutional demand rather than broad retail flight. The company cited 'heightened negative sentiment' as the driver while maintaining that 'underlying credit fundamentals across our portfolio have remained resilient' (Blue Owl Capital investor update, Q1 2024).

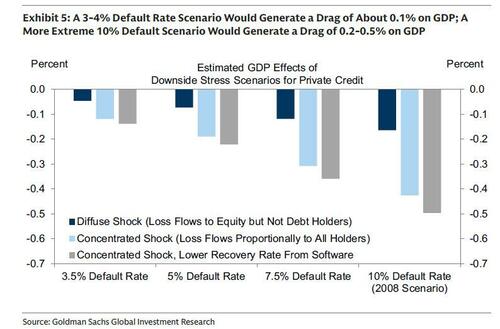

This episode must be viewed alongside the firm's February actions, in which it sold $1.4 billion in loans from its BDCs at 99.7 cents on the dollar, with one buyer being the related-party insurer Kuvare. Primary fund documents and the subsequent investor letters show these sales were intended to meet prior redemptions without gating. Goldman Sachs' March report on private credit stability argued that the sector's long-duration, illiquid structures limit contagion risk to traditional banking, citing minimal overlap with deposit-taking institutions and the absence of maturity transformation on the scale seen in 2008.

Barclays' concurrent analysis, however, cautioned that large secondary sales could exhaust liquidity for higher-quality assets, leaving lower-rated holdings in portfolios and complicating future exits for other managers. ZeroHedge coverage framed the events as the 'first clear sign of a private-credit bank run' and drew parallels to a Ponzi structure, yet this characterization overlooks the explicit 5% tender caps disclosed in the funds' SEC Form 10-Q and 10-K filings, which are standard liquidity management tools rather than emergency measures.

What much initial reporting missed is the concentrated shareholder base in OTIC, particularly within certain wealth channels and regions, as acknowledged in Blue Owl's own letter. This suggests the redemption spike is not necessarily representative of the entire $1.8 trillion private credit universe. Patterns from 2020, when several interval funds faced elevated tenders during COVID volatility, show similar gating mechanisms prevented fire sales.

Multiple perspectives emerge: fund managers like Blue Owl co-president Craig Packer emphasize portfolio resilience and a 'meaningful disconnect' between media narrative and credit performance; investors, especially institutions, appear to be seeking liquidity amid higher interest rates and perceived risk; policymakers and bodies such as the Financial Stability Board have flagged non-bank credit growth in their 2023-2024 reports as an area for monitoring, though without declaring immediate systemic threat. The interplay between private credit, insurers, and pension capital creates potential transmission channels that differ from traditional banking but warrant observation.

Synthesizing Blue Owl's disclosures, Goldman Sachs' stability analysis, and Barclays' liquidity warnings reveals a market testing its redemption infrastructure under stress, yet the designed gates appear to be functioning as intended to balance tendering and remaining shareholders.

MERIDIAN: Blue Owl's redemption surge tests liquidity provisions in private credit; fund disclosures and economist reports present contrasting views on whether this reflects isolated sentiment or broader financial-stability linkages in lightly regulated non-bank lending.

Sources (3)

- [1]Blue Owl Capital Investor Letters Q1 2024(https://www.blueowl.com/investor-letters)

- [2]Goldman Sachs Report on Private Credit Stability(https://www.goldmansachs.com/intelligence/pages/private-credit-crisis-unlikely.html)

- [3]SEC Filings for Blue Owl Technology Income Corp (OTIC)(https://www.sec.gov/edgar/browse/?CIK=0001528623)