Europe's Self-Inflicted Deindustrialization Accelerates Amid US Reshoring Push

Credible data and forecasts substantiate accelerating manufacturing job losses and firm relocation in Germany/Europe due to high energy costs, green policies, and external shocks, set against US private-sector job gains, government downsizing, and high-profile reshoring announcements under deregulation-focused leadership. The pattern reveals policy-driven capital reallocation rarely synthesized as a unified deindustrialization-versus-reshoring dynamic.

While mainstream coverage often treats Europe's economic malaise and America's manufacturing rhetoric as separate stories, a clearer pattern emerges when viewed together: divergent policy choices on energy, regulation, and industrial strategy are producing contrasting trajectories. Germany and the broader Eurozone continue to experience structural decline in core manufacturing sectors, while the US under the current administration touts a resurgence in private investment and onshoring, backed by deregulation and government downsizing.

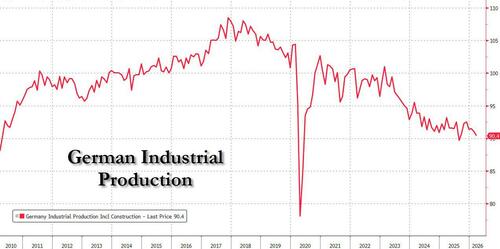

Data from 2025 shows Germany lost 248,000 jobs in key industrial sectors including motor vehicles, machinery, chemicals, and fabricated metals, with the automotive sector alone shedding 111,000 positions. Capacity utilization in some base chemicals fell to 70%, prompting prolonged shutdowns. Multiple surveys indicate that a majority of large German firms are either relocating production or scaling back domestically, driven by persistently high energy costs, regulatory burdens, and competition from subsidized Chinese exports. Official forecasts reflect this weakness: after years of recession or near-zero growth, German GDP is projected to expand by only 0.6% in 2026, with manufacturing output continuing to lag and job losses in industry offset primarily by public sector and services hiring.

This aligns with warnings of "creeping deindustrialization" from German industry groups, where the post-2022 energy shock, accelerated green transition targets, and fiscal constraints have compounded competitiveness issues. Exports have stagnated amid US tariffs and geopolitical shifts, while domestic investment remains subdued. EU economic projections similarly anticipate weak growth, rising unemployment risks, and manufacturing contraction partially masked by public services expansion.

In contrast, US policy has emphasized private-sector dynamism. The federal government shed approximately 274,000 jobs in 2025 alongside state-level cuts, contributing to a leaner public apparatus. Private sector employment showed net gains, with administration releases highlighting record reshoring announcements—including major commitments from tech giants for domestic chip, vehicle, and advanced manufacturing facilities. White House tallies describe a "largest reshoring wave in American history," linking it to tariffs, tax incentives, and reduced regulatory hurdles in energy and permitting. While independent analyses note mixed results (with some cleantech projects paused after policy shifts away from green subsidies and questions around the scale of actual on-the-ground construction), the directional contrast with Europe is evident. Higher US interest rates have been sustained without derailing momentum, partly due to perceived economic robustness and innovations in private money creation via stablecoins.

The deeper connection missed in fragmented reporting is the policy feedback loop: Europe's ideologically driven "eco-socialism"—rapid decarbonization without adequate baseload alternatives or fiscal flexibility—has raised input costs and deterred capital, accelerating firm exodus toward the US and other jurisdictions. America's approach, prioritizing energy abundance, deregulation, and private enterprise, appears to be redirecting global investment flows. This is not mere cyclical divergence but a potential structural realignment in global industrial geography, with chemicals, autos, and metals as canaries. Without course correction on energy affordability and regulatory burden, Europe's trajectory risks becoming entrenched, while US gains—though uneven—signal a quiet investment boom that rewards policy pragmatism over green dogma. Sources confirm both the severity of German industrial contraction and the US emphasis on manufacturing repatriation, painting a coherent transatlantic split.

LIMINAL: This transatlantic industrial split risks becoming semi-permanent; Europe's green regulatory overhang may accelerate talent and capital flight to the US, forcing Berlin and Brussels into emergency policy reversals or long-term secondary status in heavy industry and advanced manufacturing.

Sources (5)

- [1]German Deindustrialization Is Self-Inflicted(https://jacobin.com/2026/03/germany-deindustrialization-trade-green-elite)

- [2]Germany Has an Escalating Deindustrialisation Problem(https://internationalbanker.com/finance/germany-has-an-escalating-deindustrialisation-problem/)

- [3]Trump Effect: American Manufacturing Is Roaring Back as Factory Activity Hits Four-Year High(https://www.whitehouse.gov/releases/2026/04/trump-effect-american-manufacturing-is-roaring-back-as-factory-activity-hits-four-year-high/)

- [4]Job Growth in the Private-Sector, Massive Job Losses at Federal & State Governments in H2 2025(https://wolfstreet.com/2026/01/09/job-growth-in-the-private-sector-massive-job-losses-at-federal-state-governments-in-h2-2025/)

- [5]Economic forecast for Germany(https://economy-finance.ec.europa.eu/economic-surveillance-eu-member-states/country-pages/germany/economic-forecast-germany_en)