Petrochemical Supply Shock Exposes Global Manufacturing Fault Lines as Asian Factories Idle

Unfolding petrochemical shortages from Middle East disruptions are idling Asian textile and packaging plants faster than anticipated, exposing concentrated global supply chain vulnerabilities, historical parallels, and inflation risks overlooked by mainstream energy reporting.

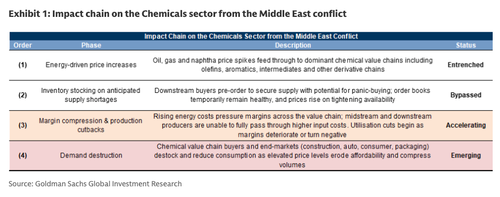

Goldman Sachs analysts led by Georgina Fraser, as reported by ZeroHedge on Monday, document that the petrochemical supply shock stemming from Middle East conflict is transmitting faster than modeled, with textile and packaging sectors in Asia already experiencing production cuts, margin compression, and early demand destruction. Spot PTA prices have risen over 30% since the onset of U.S.-Iran tensions, China's PTA capacity (roughly 75% of global supply) has seen 15% idled, and Surat's synthetic textile hub in India has shifted to single 12-hour shifts as petrochemical inputs driving 50-65% of apparel COGS deliver an implied 17% cost shock. MEG and PTA force majeure declarations have compounded tanker disruptions through the Strait of Hormuz, directly affecting PET and polyester production essential to bottles, clothing, and packaging.

This coverage effectively traces the initial transmission from Gulf energy shocks but understates structural vulnerabilities and misses longer-term patterns visible in primary sources. The IEA's 'The Future of Petrochemicals' (2018, with subsequent Oil Market Reports) establishes that petrochemicals represent the largest driver of future oil demand growth, with production highly concentrated in Asia and feedstock-dependent on Middle East stability—dynamics echoed in the 2019 Strait of Hormuz incidents and the 2021 U.S. Gulf Coast freeze that removed 20% of North American ethylene capacity. JPMorgan's commodity transmission framework, referenced in the ZeroHedge piece, correctly sequences Asia as the first impacted region yet underweights feedback loops: European chemical producers (BASF, LyondellBasell) sourcing Asian intermediates now face compounded pressure, while African and European downstream effects remain under-analyzed in mainstream reporting.

Mainstream outlets (Reuters, Bloomberg) have centered coverage on Brent crude benchmarks and tanker insurance spikes but largely omitted downstream idling of factories and the concentration risk in China's PTA dominance. They incorrectly assumed rapid unwinding post-ceasefire; primary shipping data from Vortexa and logistics assessments indicate inventory rebuilds and vessel repositioning will require 3-6 months even if Hormuz flows normalize. What remains unaddressed is how this event exposes just-in-time manufacturing's fragility—a pattern repeated from COVID-19 semiconductor and resin shortages—amplifying risks to global inflation transmission into consumer staples.

Multiple perspectives emerge from industry and policy voices. Chinese state planning documents emphasize strategic reserves and alternative olefin routes to stabilize PTA/MEG, while Indian textile associations have called for duty adjustments to protect employment. Western analysts highlight opportunities for U.S. Gulf Coast producers, yet IEA data cautions that reallocating global capacity cannot offset near-term shortages without price signals that cascade into food, beverage, and apparel inflation. This shock, viewed through the lens of concentrated chokepoints (Hormuz, Malacca Strait, and Asian refining clusters), signals deeper supply-chain risks that mainstream geopolitical coverage has yet to fully integrate, potentially accelerating corporate decisions on friend-shoring and diversified feedstock contracts.

MERIDIAN: This petrochemical shock is accelerating corporate reevaluation of single-region feedstock reliance; expect measurable shifts toward diversified sourcing and regionalized plastics production within 12-18 months even if conflict de-escalates.

Sources (3)

- [1]Petrochemical Supply Shock Begins Idling Asian Factories(https://www.zerohedge.com/geopolitical/petrochemical-supply-shock-begins-idling-asian-factories)

- [2]The Future of Petrochemicals(https://www.iea.org/reports/the-future-of-petrochemicals)

- [3]Oil Market Report November 2023(https://www.iea.org/reports/oil-market-report-november-2023)