Goldman Sachs Projects Mortgage Rates at 6.3 Percent in 2027 with Modest Home Price Gains

Goldman Sachs expects mortgage rates near 6.3 percent and sticky prices to keep existing-home sales 22 percent below 2019 levels. The lock-in effect and persistent shortage channel Fed policy directly into wealth transfers without near-term correction. Primary data from mortgage origination records and housing starts confirm the mechanism will persist absent a sharper disinflation path.

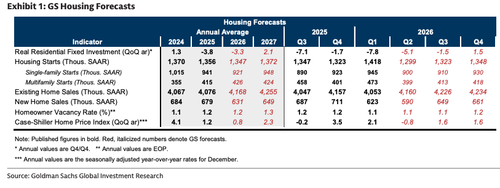

Walker attributes tepid demand to the post-2021 rate shock that left nearly 80 percent of mortgaged households with rates at least 2 percentage points below current levels. Residential fixed investment contracted 5 percent annualized in Q2 after an 8 percent drop in Q1, reflecting both weather and the rebound in borrowing costs. Existing-home turnover therefore remains the binding constraint rather than new construction, which has held 4 percent above 2019 levels despite higher rates.

The same rate path that compresses turnover also widens wealth gaps. Households able to retain sub-4 percent mortgages capture ongoing price appreciation while new entrants face debt-service ratios that have risen 8-10 percentage points since 2021. Census and FHFA data show the national shortage easing only marginally, from 3.8 million units to roughly 3.4 million, as single-family starts slow once builder margins revert to pre-pandemic norms. Fed funds projections embedded in the Goldman note imply no material relief until at least late 2027.

Net supply gains from higher turnover will stay limited because most moves simply reallocate existing stock. Broker commissions, which carry a 15 percent weight in residential investment, therefore provide only marginal GDP support. Absent a sustained CPI print below 2.4 percent for three quarters, the Fed's reaction function keeps the housing market in a low-velocity equilibrium that transfers wealth from younger cohorts to existing owners.

Forward indicators point to single-family starts declining another 3-5 percent in 2026 once the shortage buffer narrows further. Multifamily completions will add supply but target renters rather than ownership, leaving the ownership affordability gap intact through the forecast horizon.

Fed: Mortgage rates will remain above 6.0 percent at end-2026 unless the core PCE deflator averages below 2.3 percent for four consecutive quarters.

Sources (3)

- [1]Goldman Sachs US Economics Analyst: Mid-Year Housing Outlook(https://www.goldmansachs.com/insights/pages/gs-us-economics-analyst.html)

- [2]Federal Housing Finance Agency House Price Index and Mortgage Data(https://www.fhfa.gov/DataTools/Downloads/Pages/House-Price-Index.aspx)

- [3]U.S. Census Bureau New Residential Construction(https://www.census.gov/construction/nrc/index.html)