Kraft Heinz CEO's Warning Signals Deeper Economic Strain for U.S. Consumers Amid Inflation and Geopolitical Risks

Kraft Heinz CEO Steve Cahillane’s warning about consumers running out of money reflects broader economic strains from inflation, stagnant wages, and geopolitical risks like the Iran conflict. Beyond corporate earnings concerns, this article analyzes systemic issues—wage-price gaps, corporate pricing strategies, and declining savings rates—using data from the Federal Reserve and BEA. It critiques the original coverage for missing structural drivers and explores potential policy and corporate responses to avert a consumer-led slowdown.

Kraft Heinz CEO Steve Cahillane’s stark warning that consumers are 'literally running out of money toward the end of the month'—as reported in a recent Wall Street Journal interview—underscores a growing divide in the U.S. economy. While tech sectors, particularly AI-driven industries, report robust growth, the traditional consumer base, which drives 70% of U.S. GDP, faces mounting pressures from inflation, stagnant wages, and geopolitical shocks. Cahillane’s comments, echoed by executives at McDonald’s, Whirlpool, and Dine Brands, highlight a K-shaped recovery where lower-income households are disproportionately squeezed, dipping into savings and racking up credit card debt to sustain spending. This article delves beyond the surface of these corporate warnings to explore the structural and geopolitical factors exacerbating consumer distress, identifies gaps in the original coverage, and contextualizes the issue within broader economic patterns.

The original ZeroHedge piece, while alarmist in tone, captures the immediate concern of declining consumer sentiment, citing the University of Michigan’s record-low consumer confidence index. However, it misses critical systemic drivers behind this trend, such as the persistent wage-price spiral and the long-term erosion of purchasing power. Inflation, running at 3.2% as of the latest Bureau of Labor Statistics report (March 2024), has outpaced wage growth for most low- and middle-income workers, with real wages declining by 1.3% since 2021 according to the Economic Policy Institute. This gap forces households to lean on credit, as evidenced by the Federal Reserve’s data showing a $10 billion increase in credit card debt in February 2024, the highest monthly jump since the same period last year. What the original coverage also overlooks is the historical parallel to the late 1970s, when stagflation similarly crushed consumer spending power, leading to a prolonged period of economic malaise. Unlike then, today’s consumers face additional burdens from student debt (averaging $37,000 per borrower per the Federal Reserve) and housing costs, which have surged 20% since 2020 per Zillow data.

Geopolitical instability, particularly the ongoing conflict involving Iran, adds another layer of pressure not fully unpacked in the initial report. Gas prices, now averaging $4.56 per gallon per the American Automobile Association, are at their highest since July 2022, directly impacting discretionary spending for low-income households. Whirlpool CEO Marc Bitzer’s comparison of current demand drops to the 2008 financial crisis, as noted in the source, may be hyperbolic, but it signals real fear of a cascading effect. The U.S. Energy Information Administration (EIA) projects that sustained Middle East tensions could push oil prices to $100 per barrel by Q3 2024, a scenario that would further erode consumer budgets and potentially tip the economy into recession if paired with Federal Reserve rate hikes aimed at curbing inflation. This risk is under-discussed in the original piece, which focuses more on immediate sentiment than long-term structural threats.

Another missed angle is the corporate response to these consumer headwinds. While Kraft Heinz and others lament shrinking budgets, their own pricing strategies—often outpacing inflation to protect margins—contribute to the problem. Kraft Heinz raised prices by 3.6% in 2023 alone, per their Q4 earnings report, even as input costs stabilized, a move mirrored across the packaged goods sector. This 'greedflation' narrative, supported by a 2023 study from the Federal Reserve Bank of Kansas City showing corporate markups as a key inflation driver, suggests a feedback loop where companies pass costs to consumers who can least afford them, further depressing demand. The original coverage frames corporations as passive observers of consumer pain, ignoring their active role in perpetuating it.

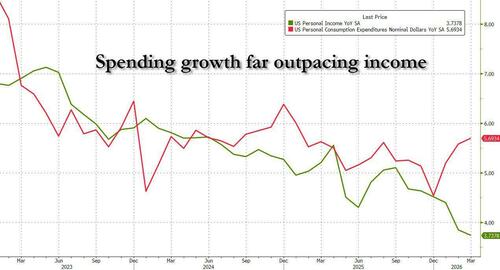

Synthesizing additional sources, the Federal Reserve Bank of New York’s recent research on gasoline consumption (March 2024) confirms that low-income households are already cutting back on fuel use, a leading indicator of broader spending retrenchment. Meanwhile, the Bureau of Economic Analysis (BEA) reported a personal savings rate drop to 3.6% in March 2024, the lowest in three years, signaling that the buffer many Americans relied on post-pandemic is nearly exhausted. These data points, combined with Cahillane’s comments, paint a picture of an economy teetering on the edge of a consumer-led slowdown, a risk amplified by external shocks like the Iran conflict.

Looking ahead, the interplay between domestic policy and global events will be critical. The Federal Reserve’s balancing act—raising rates to tame inflation while avoiding a hard landing—remains fraught, especially as geopolitical risks drive commodity price volatility. Unlike the original source’s focus on immediate corporate earnings impacts, the deeper story lies in whether these pressures will force a policy pivot, such as targeted fiscal relief for lower-income households, or accelerate a shift in corporate strategy toward value offerings. Historical patterns, like the consumer pullback during the 2008 crisis, suggest that without intervention, spending cuts could ripple through retail and hospitality, sectors already showing strain per Dine Brands’ and McDonald’s reports.

In sum, Kraft Heinz’s warning is not just a corporate soundbite but a symptom of deeper economic fissures—wage stagnation, inflationary pricing, and geopolitical instability—that threaten the U.S. consumer engine. The original coverage, while highlighting acute pain points, misses these structural undercurrents and the potential for a feedback loop between corporate actions and consumer behavior. As savings dwindle and debt mounts, the question remains: how long can Americans keep spending before the bottom truly falls out?

MERIDIAN: I anticipate that sustained high gas prices and inflation could force a consumer spending retrenchment by Q4 2024, potentially pushing the Federal Reserve to pause rate hikes if recession risks mount.

Sources (3)

- [1]Kraft Heinz CEO Interview with WSJ via ZeroHedge(https://www.zerohedge.com/economics/kraft-heinz-ceo-consumers-are-literally-running-out-money-toward-end-month)

- [2]Federal Reserve Bank of New York: Gasoline Consumption Trends(https://www.newyorkfed.org/research/policy/gasoline-consumption)

- [3]Bureau of Economic Analysis: Personal Savings Rate Data(https://www.bea.gov/data/income-saving/personal-saving-rate)