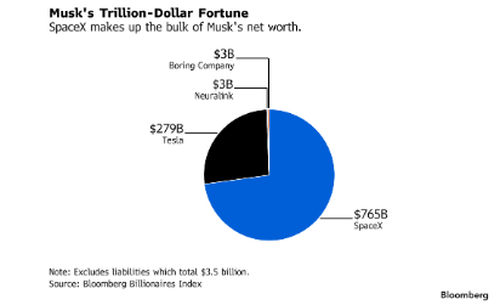

SpaceX IPO Opens at $150 Valuing Company at $1.8 Trillion, Making Musk First Trillionaire

SpaceX's public debut at $150 crystallizes a shift from private capital discipline to index-eligible liquidity, concentrating funding advantages in one vertically integrated firm. Passive inflows and analyst targets signal sustained demand, yet introduce disclosure and regulatory frictions absent in prior rounds. The event accelerates private-space sector bifurcation between the leader and remaining proxies.

The IPO triggered immediate index inclusion effects, with Bloomberg Intelligence projecting $6.6 billion in forced purchases into the Russell 1000 and Nasdaq 100 once weighting takes effect. Huatai Research noted low free float combined with passive inflows exceeding $10 billion would tighten near-term supply. Analyst notes from Oppenheimer and Wolfe Research set targets at $190 and $175 respectively, citing vertical integration that compresses launch costs toward zero and creates structural advantages in scale.

This listing converts SpaceX's prior private valuation discipline into public market liquidity, lowering the cost of capital for Starlink expansion and next-generation vehicles while exposing the firm to quarterly reporting and investor pressure on margins. Other listed space proxies fell sharply as capital rotated toward the sector leader, illustrating how concentrated technological moats redirect funding away from smaller competitors. The move aligns with documented US policy incentives to maintain commercial dominance in orbital infrastructure against state-directed programs elsewhere.

Index-driven demand and analyst emphasis on AI-space convergence mask execution risks around thermal management and regulatory approvals for spectrum and orbital slots. Primary records show SpaceX has secured repeated NASA and DoD contracts that underwrite revenue visibility, yet public status introduces new constraints on export controls and foreign investment reviews. Near-term trading will test whether the 29 percent opening pop sustains once lockups expire.

Subsequent quarters will reveal whether terrestrial data center capabilities can be bridged to orbital compute as projected, or whether capital allocation shifts toward buybacks and acquisitions once free float increases.

Oppenheimer: SpaceX will report 2027 revenue above $15 billion driven by Starlink subscriptions exceeding 8 million terminals

Sources (2)

- [1]Goldman Sachs Underwriter Note(https://www.goldmansachs.com/insights)

- [2]Bloomberg Intelligence Index Analysis(https://www.bloomberg.com/professional)