Record-High Private Credit Defaults Signal Mounting Leverage Risks Amid $2T Sector Strain

Fitch-confirmed record 6% private credit defaults in May 2026, with redemption surges at BlackRock, Blackstone, and Partners Group, point to leverage risks and possible crunch in the $2T market.

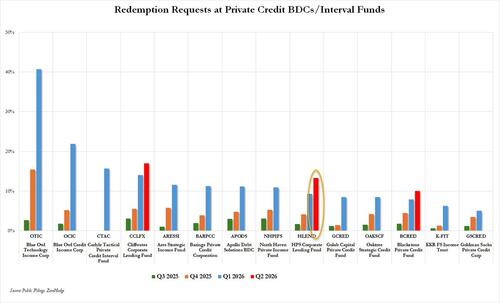

Fitch Ratings reports that the U.S. private credit default rate (PCDR) held steady at a record 6.0% for the trailing twelve months ended May 2026, unchanged from April when it first peaked at that level—the highest since Fitch began tracking in August 2024. The agency monitored roughly 1,500 issuers and recorded 14 default events in May, concentrated in healthcare, business services, and industrial manufacturing. Half involved stressed maturity extensions, often pushing terms out by one to two years. Serial defaulters accounted for six of the events. This builds on an upward trend, with the rate rising from 5.4% in February to 5.8% in January and continuing higher amid elevated interest rates. Broader context reveals redemption pressures at major players: BlackRock's private credit fund saw repurchase requests exceed 13% of shares in Q2, surpassing its 5% limit; Blackstone capped withdrawals at its flagship fund; and Partners Group halted redemptions at 5% after requests hit nearly 10%. The $2 trillion sector's exposure to software (up to 20% of loans) and middle-market borrowers amplifies vulnerabilities, with smaller EBITDA firms showing default rates over 10%. Forbes notes these defaults are testing banks and insurers, while CNBC links the surge to soaring rates. Systemic risk debates persist, but the data highlight hidden leverage and potential credit tightening overlooked by equity markets. Maturity extensions under stress now outpace other default types, suggesting borrowers are kicking the can down the road rather than resolving underlying issues.

LIMINAL: Persistent 6% defaults and maturity extensions could foreshadow tighter lending standards and spillover into broader credit markets by late 2026, pressuring leveraged borrowers beyond equity visibility.

Sources (5)

- [1]Fitch Ratings’ U.S. Private Credit Default Rate Remains at Record High 6.0% in May 2026(https://www.fitchratings.com/research/corporate-finance/fitch-ratings-us-private-credit-default-rate-remains-at-record-high-6-0-in-may-2026-15-06-2026)

- [2]Fitch Ratings’ U.S. Private Credit Default Rate Hits a High of 6.0% in April 2026(https://www.fitchratings.com/research/corporate-finance/fitch-ratings-us-private-credit-default-rate-hits-high-of-6-0-in-april-2026-18-05-2026)

- [3]Rising Private Credit Defaults Are Testing Banks And Insurers(https://www.forbes.com/sites/mayrarodriguezvalladares/2026/05/24/rising-private-credit-defaults-are-testing-banks-and-insurers/)

- [4]Private credit defaults hit record high as interest rates soar(https://www.cnbc.com/2026/05/21/private-credit-defaults-hit-record-high-as-interest-rates-soar.html)

- [5]Fitch’s Private Credit Default Rate Hits an Almost Two-Year High(https://www.wsj.com/livecoverage/stock-market-today-dow-sp-500-nasdaq-05-18-2026/card/fitch-s-private-credit-default-rate-hits-an-almost-two-year-high-goTevzzaGO8fEO38QQIS)